Prologue

- Banking credit growth refers to the rate at which the total amount of money that banks lend to borrowers increases over a specific period.

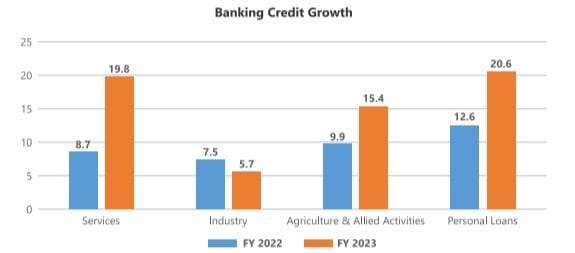

- In India, banking credit growth has been relatively strong in recent years. In FY 2023, banking credit growth was 15.4%, which was driven by strong credit off take across all sectors, including agriculture and allied activities, services, and industry.

- Banking credit growth in FY 2023 was significantly higher than in FY 2022, at 15.4% compared to 9.6%.

Banking Credit Growth in FY 2023

Banking credit growth is the annual percentage change in the total outstanding loans of commercial banks. It is an important indicator of the health of the economy, as it reflects the level of investment and economic activity. Strong banking credit growth is generally considered to be a positive sign for the economy, as it indicates that businesses are confident about the future and are willing to invest.

Banking credit growth in FY 2023 was robust, at 15.4%. This was driven by strong credit offtake across all sectors, including agriculture and allied activities , services, and industry. Banking credit growth can encompass various types of loans, including consumer loans, mortgages, business loans, and more.

The Reserve Bank of India’s (RBI) monetary policy stance is also expected to support credit growth. The central bank has kept the repo rate unchanged at 4% since May 2020, which has resulted in lower lending rates for borrowers. This has led to increased demand for credit, particularly in the retail and housing segments.

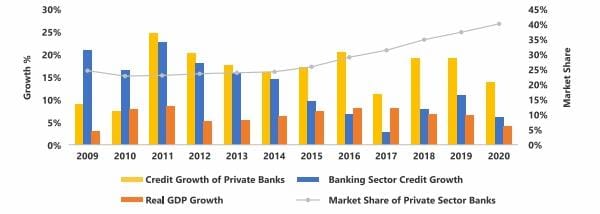

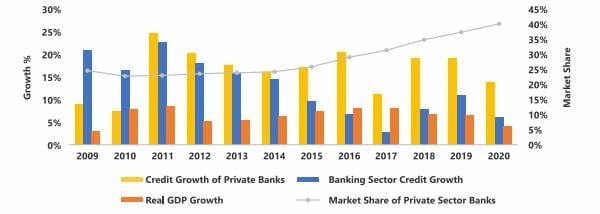

The about chart tells us that Credit growth of private banks has been gradually increasing, while the overall banking sector credit growth rate has been gradually declining also the Market share of private sector banks has been constantly increasing over the year and the real GDP growth has been at constant rate between 5% to10%.

Comparing Credit Growth with FY2022 in various Sectors

The services sector led the way in terms of credit growth, as businesses continued to invest in expansion and modernization. Credit to the agriculture and allied activities sector also grew at a healthy pace, reflecting the government’s focus on boosting agricultural production. Credit growth to the industry sector was relatively subdued, but this was due to a number of factors, including the ongoing global economic slowdown and the rising cost of capital.

When banking credit growth is high, it typically indicates that banks are extending more loans to individuals and businesses.

This can stimulate economic activity, as businesses have more capital to invest and consumers have more purchasing power.

However, excessive credit growth can also lead to concerns about inflation and financial stability if it’s not managed carefully.

Conversely, when banking credit growth is low, it may signal a cautious approach by banks, which can have a cooling effect on economic growth but may also reduce the risk of financial instability. Monitoring banking credit growth is essential for policymakers, economists, and investors as it can provide insights into the health of the banking sector and the overall economy.

- Banking credit growth in FY 2023 was significantly higher than in FY 2022, at 15.4% compared to 9.6%.

- Credit growth to the services sector accelerated to 19.8 % in March 2023 from 8.7 % a year ago, due to the improved credit off take to ‘Non-Banking Financial Companies (NBFCs)’ and ‘trade’.

- Credit to industry registered a growth of 5.7 % in March 2023 as compared with 7.5 % in March 2022. Size-wise, credit to large industries rose by 3 % as compared with 2 % a year ago.

- Credit to agriculture and allied activities rose by 15.4 %in March 2023 as compared with 9.9 % a year ago.

- Personal loans registered a growth of 20.6 % in March 2023 as compared with 12.6 % a year ago, primarily driven by ‘housing loans’.

These are some of the Factors affecting Credit growth :

- Economic Conditions : The overall health of the economy, including factors like GDP growth, inflation rates, and unemployment, can significantly impact credit growth. A booming economy often leads to higher credit demand.

- Interest Rates : Central bank policies that influence interest rates can have a direct effect on borrowing costs. Lower interest rates tend to stimulate borrowing and credit growth, while higher rates can discourage borrowing.

- Regulatory Environment : Banking regulations, including capital requirements and lending standards, can either encourage or restrict credit expansion. Stringent regulations may limit banks’ ability to lend, while more relaxed rules can stimulate lending.

- Government Policies : Government initiatives, such as stimulus programs, tax policies, and subsidies, can impact credit growth by influencing the financial capacity of individuals and businesses.

- Technological Advancements : Innovations in financial technology (Fintech) can change the lending landscape. Online lending platforms and digital payment systems can make credit more accessible and convenient.

- Market Competition : The competitive landscape in the banking sector can affect credit growth. Intense competition may lead banks to offer more attractive lending terms to attract borrowers.

Non-Performing Assets (NPA) Overview

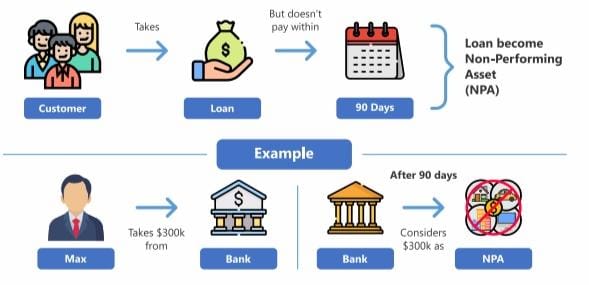

A “Non-Performing Asset” (NPA) is a financial term used in the banking and finance industry to refer to an asset, typically a loan or advance, that has stopped generating income for the lender because the borrower has defaulted on the agreed-upon payments or interest for a specific period.

The RBI defines an NPA as a loan or an advance where the interest or the installment of principal remains overdue for a period of 90 days or more. As of March 31, 2023, the gross NPA ratio of the Indian banking sector stood at 7.5%, which is a marginal improvement from the previous year’s figure of 7.8%. The net NPA ratio was 3.1%, which is a slight improvement from the previous year’s figure of 3.3%.

However, the banking sector may continue to face challenges in managing non-performing assets (NPAs). The RBI’s Financial Stability Report (FSR) has highlighted the potential risks to asset quality due to the impact of the pandemic on borrowers’ ability to repay loans. The banking sector will need to continue to focus on improving their asset quality and risk management practices to ensure sustainable credit growth in the long term.

Banks usually categorize loans as nonperforming after 90 days of nonpayment of interest or principal, which can occur during the term of the loan or for failure to pay principal due at maturity. The nonpayment of interest or principal reduces cash flow for the lender, which can disrupt budgets and decrease earnings. Loan loss provisions, which are set aside to cover potential losses, reduce the capital available to provide subsequent loans. Once the actual losses from defaulted loans are determined, they are written off.

For example, a mortgage in default would be considered nonperforming. After a prolonged period of non-payment, the lender will force the borrower to liquidate any assets that were pledged as part of the debt agreement. If no assets were pledged, the lender might write-off the asset as a bad debt and then sell it at a discount to a collections agency. The banking sector will need to continue to focus on improving their asset quality and risk management practices to ensure sustainable credit growth in the long term.

Non-Performing Assets (NPAs) can have a significant impact on banking credit growth in the following ways:

- Reduced Lending Capacity : Banks need to set aside provisions for NPAs, which are funds they can’t lend out. As NPAs increase, banks have less capital available for new loans, which can slow down credit growth.

- Risk Aversion : When banks experience a high level of NPAs, they often become more risk-averse. They may tighten their lending standards and become more selective in approving loans, which can limit the availability of credit to borrowers.

- Increased Interest Rates : To compensate for the risk associated with NPAs, banks may increase interest rates on loans. Higher interest rates can discourage borrowing and slow down credit growth.

- Impact on Profitability : High levels of NPAs can erode a bank’s profitability. To maintain their financial health, banks may focus on resolving NPAs rather than expanding their lending activities, which can hinder credit growth.

- Regulatory Scrutiny : Regulators closely monitor the NPA levels of banks. If NPAs exceed certain thresholds, regulators may impose restrictions on a bank’s lending activities, further constraining credit growth.

Outlook

The banking credit growth in FY 2023 has shown steady growth compared to the previous year. The growth rate is expected to continue in the coming years, driven by the government’s focus on infrastructure development and the ongoing economic recovery. However, banks need to be cautious in their lending practices to avoid the rise of Non-Performing Assets (NPAs).

The RBI has taken several measures to address the issue of NPAs, including the implementation of the Insolvency and Bankruptcy Code (IBC) and the formation of the National Asset Reconstruction Company (NARC). These steps will help in the recovery of stressed assets and reduce the burden on banks. The credit growth in FY 2023 is expected to be driven by sectors such as retail, infrastructure, and manufacturing. The retail segment is expected to witness strong growth due to the increasing demand for consumer durables and housing. The infrastructure sector is also expected to witness robust credit growth due to the government’s focus on infrastructure development. The manufacturing sector is expected to witness moderate growth due to the improving economic environment and the government’s push towards self-reliance.

Furthermore, the introduction of the loan restructuring scheme for MSMEs and individuals affected by the pandemic will provide relief to borrowers and prevent the rise of new NPAs. Overall, the outlook for the banking sector is positive, and banks must continue to focus on sustainable credit growth while maintaining a healthy asset quality.