Prologue

- India’s MSME sector faces a formal credit gap of ₹20–25 lakh crore, limiting their ability to scale. Supply Chain Financing offers faster, low-cost working capital solutions to bridge this gap.

- As of 2025, over ₹1.5 lakh crore worth of invoices have been financed through TReDS platforms like RXIL, M1xchange, and Invoicemart.

- The RBI made it mandatory for companies with turnover above ₹500 crore to register on TReDS. This move has driven higher adoption of SCF across large buyers and their MSME suppliers.

What is Supply Chain Financing (SCF)?

Supply Chain Financing (SCF) is a set of technology-driven solutions that optimize cash flow by allowing businesses to extend their payment terms to suppliers while enabling suppliers to get paid early. It involves collaboration between buyers, suppliers, and financial institutions to improve working capital efficiency across the supply chain. SCF typically uses instruments like reverse factoring, dynamic discounting, and invoice financing, allowing suppliers—often small and medium enterprises (SMEs)—to access affordable credit based on the creditworthiness of larger buyers. This not only strengthens supplier relationships but also enhances liquidity and financial stability for all parties involved.

Importance of Supply Chain Financing

- Improves Liquidity for Suppliers: SCF allows small and medium suppliers to access early payments, improving their cash flow without waiting for long credit periods.

- Strengthens Supply Chain Resilience: By ensuring timely payments, SCF reduces the risk of supply disruptions and builds stronger, more reliable supplier relationships.

- Optimizes Working Capital for Buyers: Buyers can extend their payment terms while ensuring suppliers are paid promptly, freeing up capital for strategic use.

- Supports MSMEs and Economic Stability: SCF provides much-needed financial support to MSMEs, helping them survive in challenging economic conditions and contributing to broader economic growth.

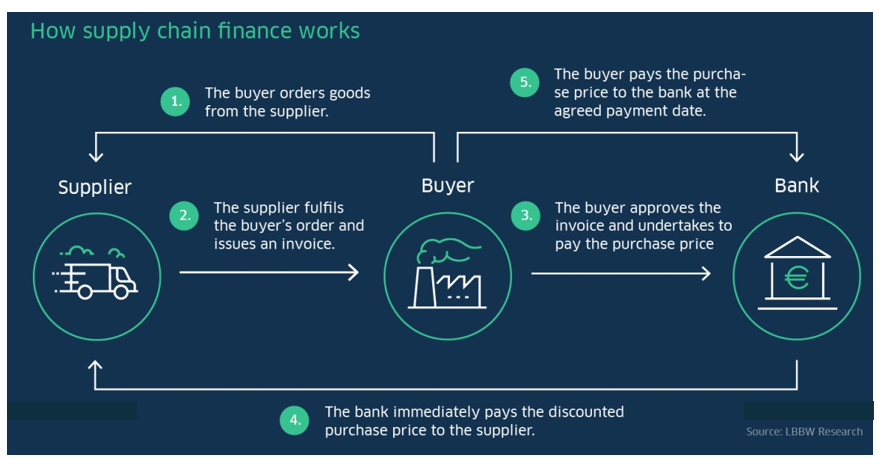

Supply Chain Financing (SCF) – Process Flow

The SCF process involves collaboration between three key parties: the buyer, the supplier, and a financing institution (usually a bank or fintech). Here’s a step-by-step overview:

- Purchase and Invoice Generation: The buyer places an order and receives goods or services from the supplier. The supplier then raises an invoice and sends it to the buyer.

- Invoice Approval by Buyer: The buyer verifies and approves the invoice, confirming the amount and due date. This approval assures the financier of the buyer’s intent to pay.

- Financing Offer by Financier: A bank or financial institution offers early payment to the supplier—typically at a discount—based on the buyer’s credit rating rather than the supplier’s.

- Early Payment to Supplier: The supplier receives the discounted payment before the due date, improving cash flow and liquidity.

- Repayment by Buyer: On the invoice due date, the buyer pays the full invoice amount to the financier, completing the cycle.

Supply Chain Finance works best when the buyer has a better credit rating than the supplier and can thus access capital from a bank or other financial provider at a lower cost. This advantage lets the buyer negotiate better terms from the supplier, such as extended payment schedules. Meanwhile, the supplier can unload its products more quickly and receive immediate payment from the intermediary financing body.

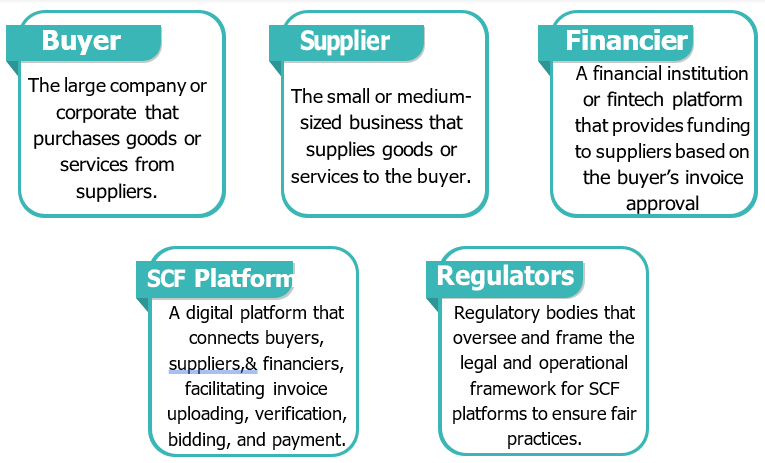

Key Participants in SCF

These participants collectively enable seamless cash flow across the supply chain, improving the financial health of all involved. The following are key participants:

Types of Supply Chain Financing

These types cater to different stages of the supply chain and address specific financing needs, helping to build a more efficient and resilient business ecosystem. The following are the types of supply chain financing:

1. Reverse Factoring (Approved Payables Financing):

A financier pays the supplier early on behalf of the buyer after the buyer approves the invoice. The buyer then repays the financier on the due date. This is buyer-led and relies on the buyer’s credit rating.

2. Invoice Discounting:

The supplier sells its unpaid invoice to a financier at a discount to get immediate funds. Unlike factoring, the buyer is usually not involved, and the supplier manages the repayment.

3. Factoring:

The supplier sells its accounts receivable (invoices) to a factoring company, which collects the payment directly from the buyer. This provides upfront liquidity and also shifts the credit risk.

4. Dynamic Discounting:

Buyers offer early payments to suppliers in exchange for a discount on the invoice amount. The earlier the payment, the higher the discount. This is funded directly from the buyer’s own liquidity.

5. Inventory Financing:

A financier provides a loan against inventory held by the supplier or buyer. This helps manage working capital while goods are in storage or transit.

6. Purchase Order (PO) Financing:

A financier funds the supplier based on the confirmed purchase order from the buyer, enabling the supplier to produce and deliver the goods before receiving payment.

7. Distributor and Dealer Financing:

Financing is provided to a buyer’s downstream partners (distributors or dealers) to help them purchase products from the manufacturer, ensuring a smoother flow of goods and cash in the supply chain.

Benefits of Supply Chain Financing

SCF creates a win-win scenario across the supply chain by improving liquidity, reducing costs, and fostering resilience. The below are some of the benefis of SCF:

Risks and Challenges of Supply Chain Financing

Addressing these challenges requires robust digital infrastructure, regulatory support, credit assessment systems, and inclusive onboarding strategies for MSMEs.

Case Studies of Supply Chain Financing

The following case studies highlight how companies across different sectors have effectively implemented SCF to improve liquidity, support suppliers, and optimize working capital:

1. Unilever – Global SCF Implementation

Overview:

Unilever, one of the world’s largest FMCG companies, implemented a global supply chain finance program to support its vast network of suppliers across more than 100 countries.

SCF Strategy:

Unilever partnered with multiple global banks to offer early payments to suppliers through reverse factoring. The program was designed to leverage Unilever’s strong credit profile to reduce the cost of capital for its suppliers.

Results:

- Over 60,000+ suppliers gained access to faster, low-cost liquidity.

- Supplier payment terms were extended without harming relationships.

- Strengthened supply chain resilience during disruptions, including COVID-19.

2. Tata Motors – Dealer & Supplier Financing

Overview:

Tata Motors launched a structured SCF program for both its suppliers and over 10,000 dealers across India, to improve liquidity and inventory turnover.

Financing Model:

Through partnerships with banks and NBFCs, Tata Motors offered dealer financing for inventory purchases and reverse factoring for suppliers. The company also integrated the system with ERP for real-time processing.

Results:

- Dealers received on-demand credit to stock vehicles efficiently.

- Suppliers had faster invoice realization and reduced borrowing costs.

- Tata Motors ensured a more stable and responsive supply chain.

Future Trends in Supply Chain Financing

- The future of Supply Chain Financing (SCF) is poised to be increasingly digital, inclusive, and data-driven. With the rapid adoption of fintech platforms and ERP integration, SCF is becoming more accessible and efficient for businesses of all sizes.

- Technologies like AI and blockchain are expected to play a critical role in enhancing transparency, risk assessment, and fraud prevention.

- Sustainability-linked financing is gaining momentum, where suppliers meeting ESG standards may receive preferential terms. Additionally, cross-border SCF solutions are set to expand, supporting global trade.

- Regulatory initiatives, especially in countries like India with platforms like TReDS, will further boost SCF adoption, while partnerships between banks and fintechs will drive innovation and scale in the financing ecosystem.

Conclusion

Supply Chain Financing (SCF) is a powerful tool that enhances liquidity, strengthens supplier relationships, and supports financial stability across the value chain. With the rise of digital platforms and regulatory support, SCF is becoming increasingly vital for businesses— especially MSMEs—to manage working capital efficiently and ensure sustainable growth.