Prologue

- Interest rates in India are primarily influenced by the Reserve Bank of India’s (RBI) repo rate, which is the rate at which the RBI lends to commercial banks.

- As of early 2025, the repo rate stands at 6.25%, following a 25 basis points reduction in February 2025 aimed at stimulating economic growth .

- The weighted average lending rate in India is projected to be around 9.65% by the end of the current quarter . Consumer spending has shown resilience, amounting to ₹24.57 trillion by the end of the second quarter of 2024.

Introduction

Interest rates play a crucial role in shaping a country’s economic landscape, influencing borrowing, spending, and overall financial stability. Set by central banks, such as the Reserve Bank of India (RBI), these rates determine the cost of loans for consumers and businesses, affecting everything from home purchases to corporate investments. When interest rates rise, borrowing becomes more expensive, leading to reduced spending and slower economic growth. Conversely, lower interest rates make credit more affordable, encouraging borrowing and boosting consumer demand.

In India, changes in the RBI’s repo rate directly impact lending and deposit rates, affecting millions of borrowers and investors. Understanding the relationship between interest rates, borrowing, and spending is essential for individuals, businesses, and policymakers to make informed financial decisions and navigate economic fluctuations effectively.

Understanding Interest Rates

Interest rates play a crucial role in finance, influencing borrowing costs and investment returns. They represent the cost of borrowing money for borrowers and the reward for saving or investing for lenders. Interest rates can be classified into different types based on how they are calculated and their impact on financial decisions.

Nominal Interest Rate:

The nominal interest rate is the stated or advertised rate on a loan or investment, without considering inflation or the effects of compounding. This rate is typically expressed as an annual percentage and is used in loan agreements, savings accounts, and bond investments.

Real Interest Rate:

The real interest rate adjusts the nominal interest rate for inflation, providing a more accurate measure of the actual return on savings or the true cost of borrowing. Inflation erodes the value of money over time, so a high inflation rate can significantly reduce the benefits of earning interest on savings.

Effective Interest Rate (EIR):

The effective interest rate (EIR), also known as the annual percentage yield (APY), takes into account the impact of compounding interest within a year. Unlike the nominal interest rate, which does not factor in compounding, the effective interest rate provides a clearer picture of how much interest is actually earned or paid over time.

Prime Rate:

The prime rate is the interest rate that commercial banks charge their most creditworthy customers, typically large corporations or well-established businesses. It serves as a benchmark for various types of loans, including personal loans, business loans, adjustable-rate mortgages, and credit cards.

Fixed Interest Rate:

A fixed interest rate remains the same throughout the loan or investment period. It provides predictability in payments and earnings, making it ideal for mortgages, car loans, and long-term investments. Fixed rates protect borrowers from interest rate fluctuations but may result in higher initial costs compared to variable rates.

Variable (Floating) Interest Rate:

A variable interest rate fluctuates based on market conditions, often tied to an index such as the LIBOR (London Interbank Offered Rate) or a central bank’s policy rate. While variable rates can offer lower initial costs, they pose risks for borrowers if rates increase.

Factors Influencing Interest Rates

Interest rates are influenced by a variety of economic, financial, and policy-driven factors. These factors determine the cost of borrowing and the return on investments. Below are the key factors that affect interest rates:

1. Inflation:

Inflation is one of the most significant factors affecting interest rates. When inflation rises, the purchasing power of money decreases, prompting central banks to increase interest rates to control inflation. Higher interest rates make borrowing more expensive, reducing spending and slowing inflation.

Example:

- If inflation is 5% and the nominal interest rate is 4%, the real return on savings is negative (-1%), discouraging saving.

- Central banks may raise rates above 5% to maintain a positive real interest rate.

2. Central Bank Policies (Monetary Policy):

Central banks, such as the Federal Reserve (USA) or the European Central Bank (ECB), set benchmark interest rates to regulate the economy. Through monetary policy tools like the repo rate, bank rate, and open market operations, they influence lending and borrowing rates.

- Expansionary Monetary Policy: Lowers interest rates to encourage borrowing and investment.

- Contractionary Monetary Policy: Raises interest rates to curb inflation and excessive economic growth.

3. Economic Growth and GDP:

Interest rates are closely linked to a country’s economic growth. During periods of strong economic growth, demand for loans increases as businesses expand and consumers spend more, leading to higher interest rates. Conversely, during economic downturns, central banks lower rates to stimulate borrowing and investment.

Example:

- If GDP growth is high, businesses require more capital, increasing the demand for loans and pushing interest rates higher.

- In a recession, borrowing demand falls, leading to lower interest rates.

4. Government Borrowing (Fiscal Policy & Public Debt):

When governments borrow heavily to fund budget deficits, they issue bonds and securities to investors. High government borrowing can lead to higher interest rates as the demand for capital increases. If investors see a country’s debt as risky, they may demand higher interest rates to compensate for the risk.

Example:

- Countries with excessive debt, like Argentina in past financial crises, faced high interest rates due to increased risk perception.

- If government borrowing is low, interest rates may remain lower.

5. Supply and Demand for Credit:

Interest rates fluctuate based on the supply and demand for credit in the financial markets.

- When demand for loans is high (business expansion, consumer credit growth), interest rates rise.

- When demand is low (economic slowdown, reduced investment activity), interest rates fall.

Example:

- During a housing boom, mortgage loan demand increases, leading to higher interest rates.

- During a crisis, people and businesses borrow less, and banks lower interest rates to attract borrowers.

Impact of Interest Rates on Borrowing

Interest rates directly affect the cost of borrowing, influencing consumer behavior, business investments, and overall economic growth. Higher interest rates make borrowing more expensive, while lower rates encourage more borrowing. Below are the key ways interest rates impact borrowing:

1. Cost of Loans and Mortgages:

Interest rates determine how much borrowers pay in interest on loans such as personal loans, home mortgages, auto loans, and student loans.

- Higher Interest Rates: Increase monthly payments, making loans more expensive and reducing affordability.

- Lower Interest Rates: Decrease monthly payments, making borrowing cheaper and encouraging more people to take loans.

Example:

- A $200,000 mortgage loan at 3% interest results in a lower monthly payment than the same loan at 6% interest, increasing home affordability.

2. Business Investments and Expansion:

Businesses rely on loans for expansion, equipment purchases, and operational growth.

- Higher Interest Rates: Increase the cost of business loans, discouraging expansion and reducing capital investments.

- Lower Interest Rates: Make borrowing cheaper, encouraging businesses to expand and invest in new projects.

Example:

- A company considering a factory expansion may delay the project if interest rates rise, making the loan too costly.

3. Consumer Spending and Credit Card Debt:

Interest rates impact credit card borrowing, personal loans, and installment payments.

- Higher Interest Rates: Increase credit card interest and discourage excessive borrowing.

- Lower Interest Rates: Encourage consumer spending, boosting retail sales and the economy.

Example:

- If credit card interest rates rise from 15% to 25%, consumers may reduce their credit usage to avoid high-interest payments.

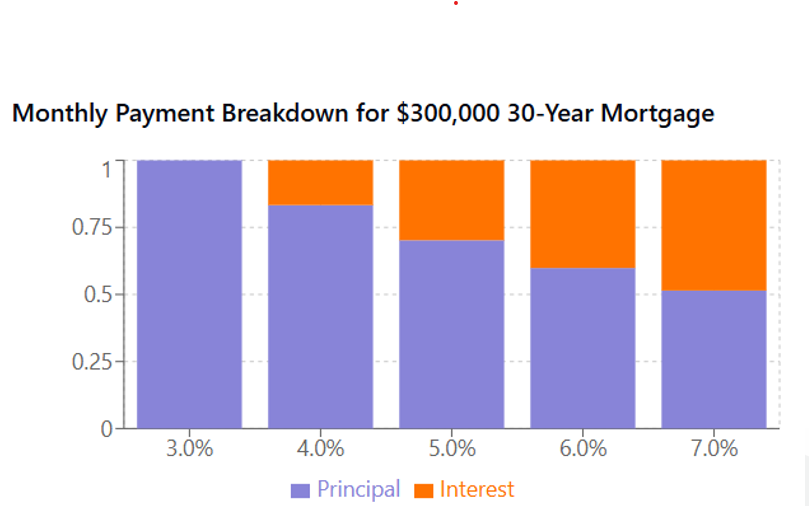

Payment Structure Analysis

- Fixed Payment Principle: For a given loan amount and term, the total payment increases with interest rates

- Payment Allocation: At 3% on a $300,000 mortgage, most of the payment builds equity; at 7%, nearly half goes to interest

- Wealth Building Impact: Higher rates significantly reduce the wealth-building potential of borrowing

As interest rates rise, a higher portion of the monthly payment goes toward interest rather than principal. At 7%, interest comprises nearly half the payment amount.

Impact of Interest Rates on Spending

Interest rates play a crucial role in influencing consumer and business spending. When interest rates rise or fall, they affect borrowing costs, disposable income, and investment decisions, ultimately shaping overall economic activity.

1. Consumer Spending:

Consumer spending is one of the largest drivers of economic growth. Interest rates influence how much people spend versus save.

Higher Interest Rates:

- Increase borrowing costs, making loans, credit cards, and mortgages more expensive.

- Reduce disposable income as loan repayments rise, leading to less spending on non-essential goods.

- Encourage saving, as higher interest rates offer better returns on deposits.

Lower Interest Rates:

- Make borrowing cheaper, encouraging consumers to take loans for cars, homes, and large purchases.

- Increase disposable income as loan repayments decrease, leading to more spending.

- Discourage saving since lower rates reduce the returns on savings accounts.

Example:

- If auto loan rates drop from 7% to 4%, more people may buy cars, boosting car sales and related industries.

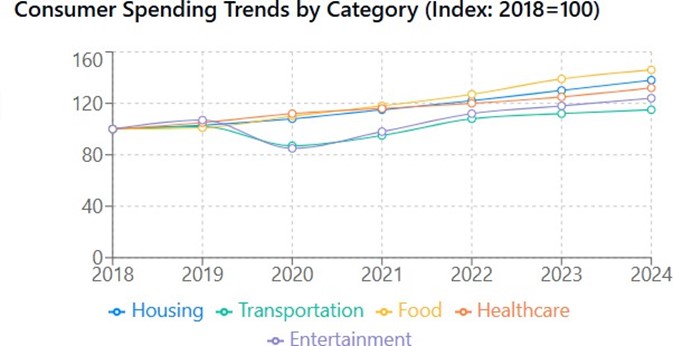

- Food Cost Acceleration: Food has seen the most dramatic increase (+46% since 2018), reflecting significant inflation in this essential category

- Housing Pressure: Housing costs have climbed steadily (+38%), creating affordability challenges

- Pandemic Effects: Transportation spending shows distinct pandemic disruption with a 13% drop in 2020 before rebounding

- Healthcare Consistency: Healthcare spending shows steady growth regardless of economic conditions, demonstrating its inelastic nature

- Entertainment Volatility: Entertainment spending dropped during the pandemic but has recovered and continued growing.

2. Housing Market and Real Estate Spending:

Interest rates strongly influence the real estate market, affecting home buyers, renters, and property investors.

Higher Interest Rates:

- Make mortgages more expensive, reducing home affordability.

- Reduce real estate investment as financing becomes costlier.

Lower Interest Rates:

- Make home loans more affordable, increasing demand for houses.

- Boost real estate investment as borrowing costs decline.

Effects of Interest Rates on Economic Sectors

Banking and Financial Services:

Banks benefit from higher interest rates as they earn more on loans, but loan demand decreases due to higher borrowing costs. Lower interest rates encourage more lending but reduce bank profit margins.

Real Estate and Housing Market:

Higher interest rates make mortgages more expensive, reducing home sales and slowing property price growth. Lower rates make home ownership more affordable, increasing demand and boosting real estate investment.

Consumer Goods and Retail:

When interest rates rise, consumers cut back on spending, especially on non-essential items, hurting retail sales. Lower rates increase disposable income, encouraging spending on electronics, furniture, and luxury goods.

Automotive Industry:

Higher interest rates make auto loans expensive, lowering car sales. Lower rates boost vehicle purchases by making financing more affordable, benefiting automakers and dealerships.

Manufacturing and Industrial Sector:

Factories and businesses rely on loans to expand. Higher interest rates raise production costs, reducing investments. Lower rates make financing cheaper, encouraging industrial growth and exports.

Effects of Interest Rates on Economic Sectors

Banking and Financial Services:

Banks benefit from higher interest rates as they earn more on loans, but loan demand decreases due to higher borrowing costs. Lower interest rates encourage more lending but reduce bank profit margins.

Real Estate and Housing Market:

Higher interest rates make mortgages more expensive, reducing home sales and slowing property price growth. Lower rates make home ownership more affordable, increasing demand and boosting real estate investment.

Consumer Goods and Retail:

When interest rates rise, consumers cut back on spending, especially on non-essential items, hurting retail sales. Lower rates increase disposable income, encouraging spending on electronics, furniture, and luxury goods.

Automotive Industry:

Higher interest rates make auto loans expensive, lowering car sales. Lower rates boost vehicle purchases by making financing more affordable, benefiting automakers and dealerships.

Manufacturing and Industrial Sector:

Factories and businesses rely on loans to expand. Higher interest rates raise production costs, reducing investments. Lower rates make financing cheaper, encouraging industrial growth and exports.

Conclusion

Interest rates play a pivotal role in shaping economic activities. Central banks adjust rates to balance inflation and economic growth. While low interest rates stimulate borrowing and spending, excessively low rates can lead to asset bubbles. Conversely, high rates help curb inflation but may slow down economic growth. Understanding the dynamics of interest rates helps individuals, businesses, and policymakers make informed financial decisions.