Prologue

- Infrastructure spending is expected to grow from $4 trillion per year in 2012 to more than $9 trillion per year by 2025.

- India’s infrastructure sector is poised for strong growth, with investments worth US$1.4 trillion planned by 2025 under the National Infrastructure Pipeline (NIP).

- Private industrial CapEx in India is expected to rise from Rs 4.4 lakh crore in FY24 to Rs 6.7 lakh crore in FY28, a 52% increase.

- The global semiconductor manufacturing industry alone is set to see $1 trillion in CapEx spending by 2030.

Introduction to CapEx in Infrastructure sector

- The infrastructure sector plays a critical role in economic development, requiring substantial capital expenditures (CapEx) to build and maintain assets such as transportation networks, utilities, energy systems, and urban facilities. These projects often demand significant upfront investments with extended payback periods, making effective funding strategies essential for their feasibility and sustainability.

- Capital expenditure (Capex) funding for the infrastructure sector typically involves large investments in physical assets, such as transportation systems, energy facilities, water resources, and urban development projects. Funding these projects requires robust financial models that balance public and private sector contributions, risk allocation, and long-term sustainability.

Capex Funding Models for the Infrastructure sector

Public Sector Financing:

- In this model, governments finance infrastructure projects directly through public budgets, often using tax revenues or sovereign debt. Public sector financing ensures that projects align with public welfare objectives and remain affordable to citizens.

- Turnover Time: 10–20 years (long-term due to slower payback from public funds or taxes).

- Inference: This model suits essential infrastructure (e.g., roads, schools) where social benefits outweigh financial returns. The long turnover ties up public resources, limiting concurrent large-scale projects.

- Examples: Construction of free public highways, schools, and hospitals, Government-funded rail or irrigation projects.

Private Sector Financing:

- Private sector involvement in infrastructure funding is characterized by investments from corporations or financial institutions, typically through equity or debt financing. Private companies may recover their investments via user fees, long-term contracts, or revenue-sharing models.

- Turnover Time: 5–15 years (shorter due to market-driven efficiency and high return expectations).

- Inference: Suitable for commercial infrastructure (e.g., airports, industrial parks), the shorter turnover time ensures private investors quickly recover and reinvest funds, encouraging innovation and competitive pricing.

- Examples: Privately developed renewable energy plants, Logistics hubs and commercial port facilities.

Public-Private Partnerships (PPP):

- PPPs are a collaborative funding model where risks, responsibilities, and rewards are shared between public and private entities. Common structures include Build-Operate-Transfer (BOT), where private entities develop and operate projects for a specified period before transferring ownership to the public sector, and Design-Build-Finance-Operate (DBFO), where the private sector takes on design, construction, financing, and operation roles.

- Turnover Time: 10–25 years (depending on the concession period).

- Inference: PPPs balance risk and ensure quicker capital recovery through shared investments. These are ideal for revenue-generating projects like toll roads and metro systems but require robust contracts and governance.

- Examples: Airports developed under BOT models (e.g., Delhi International Airport in India), Toll highways (e.g., Golden Quadrilateral highways in India).

Green Finance and Sustainability Funds:

- This emerging model targets environmentally sustainable infrastructure, with funding derived from green bonds, climate funds, or ESG (Environmental, Social, and Governance) investment pools. These funds attract socially responsible investors looking to align their portfolios with global climate goals. Green finance supports projects like renewable energy plants, energy-efficient buildings, and sustainable urban infrastructure.

- Turnover Time: 10–20 years (sustainability-focused projects often have longer payback periods).

- Inference: Suitable for renewable energy and eco-friendly urban projects, green bonds and ESG investments ensure alignment with global sustainability goals while diversifying funding.

- Examples: Solar energy parks funded by green bonds, Green-certified buildings in urban centers.

Hybrid Funding Models:

- Hybrid models blend multiple funding approaches to address complex project requirements. These models may combine public grants, private investments, and user charges, effectively diversifying risks and attracting broader capital sources. Hybrid financing is particularly useful for large-scale projects requiring substantial upfront investment and long-term sustainability, such as urban smart cities or large renewable energy projects.

- Turnover Time: 10–25 years (dependent on concession duration).

- Inference: Hybrid models distribute risks among stakeholders, ensuring that no single entity bears the entire burden. Public grants lower risks for private investors, while private participation enhances efficiency and accountability.

- Example: Blended finance for urban smart city initiatives.

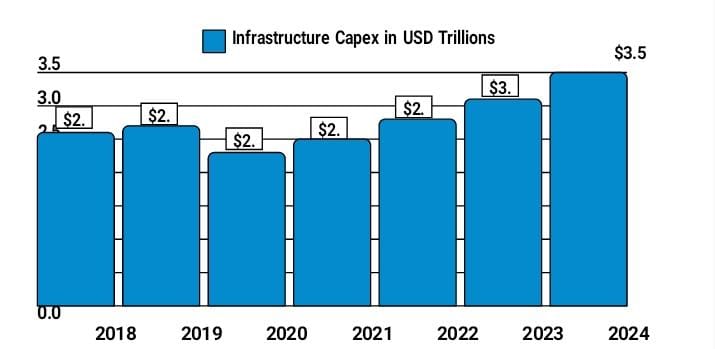

Capex Performance Analysis

From FY2017-18 to FY2023-24, infrastructure investments in India have grown exponentially, with a sharp rise in public sector outlays. In FY2023-24, capital expenditure was increased by 35.4%, totaling Rs 7.5 lakh crore, with approximately 67% spent in the first nine months of the fiscal year. The central government’s CapEx has increased from a long-term average of 1.7% of GDP (FY09 to FY20) to 2.5% of GDP in FY24.

Capital expenditure by the Government of India has seen significant growth. From FY2021-22 to FY2023- 24, annual budgetary outlays for infrastructure have increased consistently, with FY2023-24 witnessing a record allocation of ₹10 lakh crore, representing 3.3% of GDP.

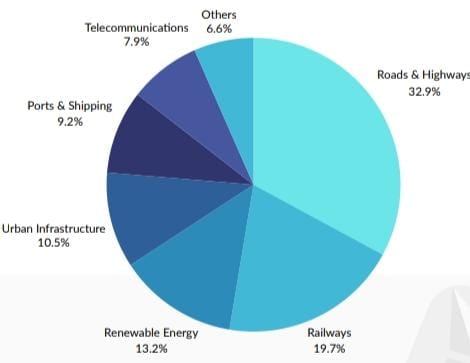

Sectoral Breakdown (Annual Capex)

Infrastructure investment in India spans across various critical sectors, with government budgets and private contributions playing significant roles. Below is the annual CapEx distribution by major infrastructure sectors, based on recent data from government allocations and reports for FY2023-24:

Introduction to CapEx in Manufacturing sector

Capital Expenditure (CapEx) in the manufacturing sector refers to the funds a company invests in acquiring, upgrading, or maintaining physical assets critical to its production processes. These assets include facilities, machinery, equipment, and technology that enable the manufacturing of goods. CapEx decisions are strategic and essential for ensuring operational efficiency, meeting production demands, and sustaining long- term business growth.

Capex Funding Models for the Manufacturing sector

Capex funding models for the manufacturing sector cater to the needs of highly capital-intensive operations such as setting up factories, procuring machinery, expanding production lines, and upgrading technology. These models balance the need for significant upfront investments with long-term financial sustainability. Below are the key funding models tailored to manufacturing sector:

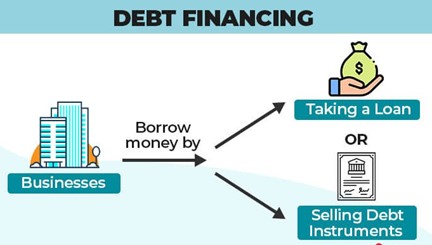

Traditional Debt Financing:

- This model involves borrowing funds through loans, bonds, or credit lines to finance capital expenditures. The borrowed amount is repaid over time with interest, allowing manufacturers to maintain cash flow while funding large projects. Debt financing is typically used for long-term investments and requires a solid credit history.

- Turnover Time: Medium to long-term (3 to 10 years)

- Inference: Debt financing allows manufacturers to access large sums of capital quickly, but its repayment obligations can strain cash flow. Interest rates, credit terms, and loan duration affect the cost. It’s suitable for companies looking for external capital without losing ownership.

- Example: Loans for purchasing heavy machinery or setting up production units.

Equity Financing:

- Manufacturers can raise capital by selling ownership stakes in the business to investors, such as venture capitalists or private equity firms. This provides funding without incurring debt, but it dilutes ownership and control. Equity investors expect returns through dividends or capital appreciation.

- Turnover Time: Long-term (5-10 years or more)

- Inference: Equity investment does not require immediate repayment and allows for flexibility in funding. However, it involves dilution of ownership and control, and investors expect significant returns over time. This is ideal for companies with high growth potential but may not be an option for smaller or less attractive companies.

Leasing and Asset Financing:

- A contractual agreement where a business (the lessee) pays a periodic fee to use an asset owned by another party (the lessor). The lease can be short-term or long-term, and is often used for high-value assets like machinery, vehicles, and equipment. Instead of purchasing equipment and machinery outright, manufacturers can lease them or use asset financing (where the equipment is used as collateral to secure a loan).

- Turnover Time: Short-term to Medium-term (1-7 years depending on the lease type)

- Inference: Good for companies needing equipment with limited upfront capital. Provides flexibility, but over time, leasing costs may exceed purchase costs.

Government Grants and Subsidies:

- Many governments offer grants, tax incentives, and subsidies for manufacturing companies, especially in areas like technology innovation, environmental sustainability, and workforce development.

- Turnover Time: Short to Medium-term (Grant periods typically range from 6 months to 3 years).

- Inference: No repayment required, but often limited to specific sectors or purposes (e.g., R&D, sustainability). Time-consuming application process.

Venture Capital:

- Venture capitalists invest in manufacturing startups with high growth potential in exchange for equity stakes. Venture capital firms provide funding to early-stage companies in return for equity and often play an active role in business strategy and management.

- Turnover Time: Long-term (Typically 3–7 years, with an exit strategy planned around 5–7 years).

- Inference: Suitable for high-growth companies looking for substantial capital. Offers expertise but results in ownership dilution and pressure for high returns. Access to significant funding, business expertise, and networking opportunities.

Manufacturing Capex Performance Analysis

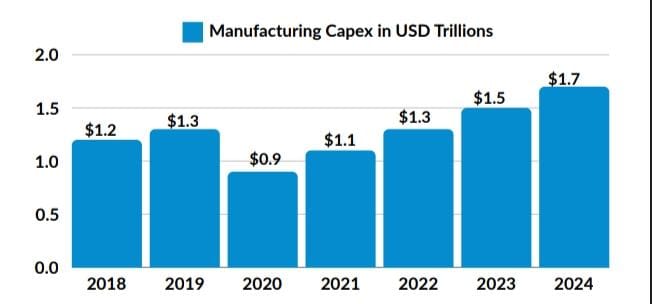

CapEx in the manufacturing sector has seen a significant rise, driven by technological advancements, modernization needs, and government initiatives like the Production-Linked Incentive (PLI) schemes. Increased CapEx has contributed to economic growth by creating jobs, enhancing production efficiency, and boosting exports. The manufacturing sector is a significant contributor to GDP and is expected to reach $1 trillion by 2025-26:

The pre-pandemic period from 2018 to 2019 demonstrated steady growth, with manufacturing capex incrementally rising from $1.2 trillion to $1.3 trillion, indicating a stable and optimistic investment environment. However, the emergence of COVID-19 in 2020 precipitated a dramatic 28% decline, with investments plummeting to $0.9 trillion, representing the most significant disruption in recent manufacturing history. The years 2022 and 2023 witnessed accelerated growth, with capex climbing to $1.3 trillion and $1.5 trillion respectively, surpassing pre-pandemic levels and indicating a robust recovery.

Challenges Faced in CapEx Funding Models

- High Capital Intensity: Infrastructure projects require significant upfront capital, making it difficult for companies to secure the necessary funding. This often results in long-term debt or reliance on government grants, which can be restrictive.

- Project Execution and Management Risks: The scale and complexity of infrastructure projects can lead to delays, cost overruns, or failure to meet quality standards. Effective project management and risk mitigation strategies are essential but challenging to maintain consistently.

- Technological Uncertainty: The rapid pace of technological advancement in manufacturing can make it difficult to predict which investments will yield the best returns. This uncertainty can deter companies from committing large sums of capital to new technologies.

- Cost Overruns and Budgeting Issues: Manufacturing CapEx projects often face unexpected cost overruns due to price volatility in materials, labor shortages, or unforeseen technical challenges. Proper forecasting and budget control can be difficult to achieve.

Conclusion:

CapEx funding models for the infrastructure and manufacturing sectors play a crucial role in driving long- term growth, operational efficiency, and innovation. For the infrastructure sector, these models face challenges such as high capital intensity, long payback periods, and regulatory complexities, which can make securing and managing funding more difficult. Similarly, in the manufacturing sector, funding for capital expenditures is hindered by cash flow constraints, technological uncertainties, and the risk of cost overruns. Despite these challenges, financing options like debt financing, leasing, and venture capital provide manufacturers with opportunities to invest in necessary technological advancements, plant expansions, and process improvements.