- In India, As of 2025, public sector banks offer MSME loans at rates starting from 8.50% to 12.00%, while NBFCs and fintechs may charge between 12% to 24% annually.

- Over 65% of MSMEs prefer flexible repayment structures to manage seasonal business fluctuations.

- Approximately 72% of MSME loans in India still require some form of collateral, as per RBI data. However, collateral-free loans under CGTMSE and fintech-led underwriting models are rising.

Introduction

Choosing the right business loan is a critical financial decision that can significantly influence a company’s growth trajectory, operational efficiency, and long-term sustainability. An ideal loan deal is not just about securing funds—it involves evaluating multiple factors such as interest rates, repayment terms, collateral requirements, lender credibility, and processing speed. For businesses, especially MSMEs and startups, aligning the loan structure with cash flow cycles and business goals is essential to avoid financial strain. In today’s dynamic lending landscape, understanding the anatomy of an ideal deal empowers entrepreneurs to make informed choices, minimize risks, and maximize the benefits of external financing.

Why Choosing the Right Business Loan Matters

Choosing the right business loan is crucial because it directly impacts a company’s financial stability, growth potential, and operational flexibility. A well-structured loan with suitable interest rates, repayment terms, and minimal hidden costs ensures that the borrowed funds serve as a catalyst for business expansion rather than a financial burden. The wrong loan— whether due to high EMIs, inflexible terms, or excessive collateral requirements—can strain cash flows, limit reinvestment, and even risk default.

- Financial Stability: The right loan structure ensures manageable EMIs and prevents cash flow disruptions, keeping daily operations smooth.

- Cost Efficiency: Selecting loans with lower interest rates and minimal hidden fees reduces the overall cost of borrowing.

- Business Growth Support: Properly matched funding helps in scaling operations, expanding markets, or investing in new assets without overburdening finances.

- Credit Health: Timely repayment of a well-planned loan boosts credit scores, improving eligibility for future funding.

- Risk Mitigation: Avoids over-leveraging and reduces the risk of default or asset loss due to unfavorable loan terms or high collateral demands.

- Flexibility & Customization: Loans tailored to business cycles (seasonal or project-based) offer better repayment flexibility, improving financial planning.

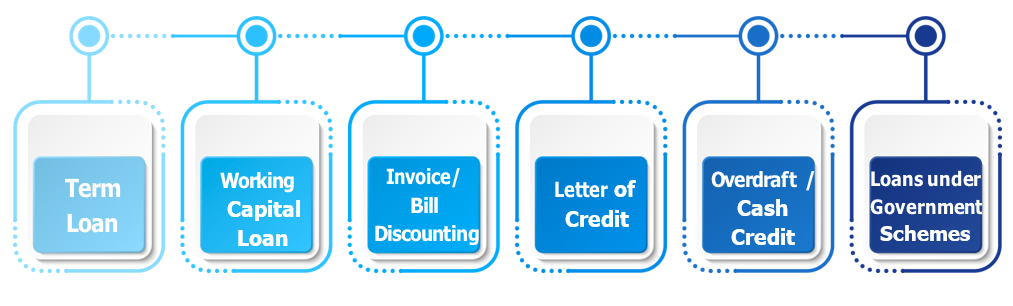

Types of Business Loans

There are various types of business loans available in the market, each designed to meet specific financial needs of different types of businesses. Below are the following types of business loans with brief explanations:

Term Loan:

A Term Loan is a lump-sum loan provided for a fixed period, typically ranging from 1 to 10 years, and repaid in regular monthly installments (EMIs). It is commonly used for funding business expansion, purchasing equipment, or long-term capital investments.

Working Capital Loan:

A Working Capital Loan is a short-term loan designed to finance a business’s everyday operational needs like inventory, salaries, rent, and utilities. It helps bridge cash flow gaps during off-seasons or delays in receivables.

Invoice/Bill Discounting:

Invoice or Bill Discounting is a short-term financing method where businesses sell their unpaid customer invoices to a lender at a discount to get immediate cash. It improves working capital by unlocking funds tied up in receivables.

Letter of Credit (LC):

A Letter of Credit is a financial guarantee issued by a bank on behalf of a buyer, assuring the seller of payment upon fulfillment of specific terms, usually in international trade. It reduces the risk of default for exporters by ensuring the bank pays if the buyer fails to do so.

Overdraft / Cash Credit:

Overdraft (OD) or Cash Credit (CC) is a flexible short-term loan facility where businesses can withdraw funds beyond their account balance, up to a sanctioned limit. Interest is charged only on the amount utilized, not the full limit.

Loans under Government Schemes:

These are specially designed loan programs supported by the Indian government to promote entrepreneurship, especially among MSMEs, startups, and underserved sectors. Schemes like Mudra (for micro-units), CGTMSE (collateral-free MSME loans), and PMEGP (for new entrepreneurs) offer lower interest rates, relaxed eligibility, and sometimes subsidy benefits.

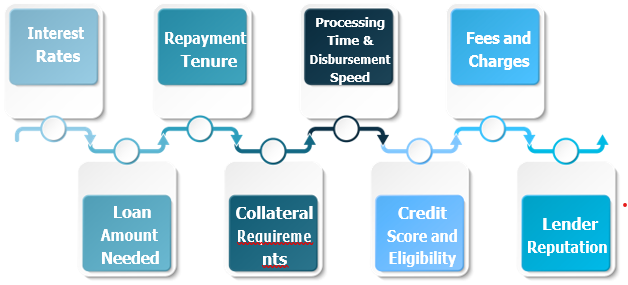

Key Considerations While Choosing a Business Loan

Here is a detailed explanation of the Key Considerations While Choosing a Business Loan, covering every aspect a business should evaluate to make an informed and financially sound decision:

- Interest Rate: The interest rate determines the total cost of the loan over its tenure. It’s essential to compare offers from banks, NBFCs, and fintechs to find the most competitive rate. Even a 1–2% difference can significantly impact the total repayment amount over time.

- Loan Amount Needed: Borrow only what your business genuinely requires based on current needs and projected expenses. Over-borrowing increases repayment pressure, while under-borrowing may hinder growth or operational stability. A clear assessment of use of funds is crucial.

- Repayment Tenure: The loan tenure affects both EMI amount and total interest paid. A longer tenure reduces monthly burden but increases total cost, while a shorter one saves on interest but may strain monthly cash flow. Choose a tenure aligned with your business cycle.

- Collateral Requirements: Understand whether the loan requires you to pledge assets such as property, machinery, or inventory. Secured loans often offer lower interest but carry the risk of asset loss on default. Unsecured loans are faster but usually more expensive.

- Processing Time & Disbursement Speed: Some lenders, especially fintechs and NBFCs, disburse loans within 24–72 hours, while traditional banks may take weeks. Speed is crucial if your business needs funds urgently for orders, working capital, or emergencies.

- Fees and Charges: Besides interest, consider processing fees, late payment charges, prepayment penalties, and foreclosure fees. These hidden costs can add up quickly and make a loan more expensive than it appears initially.

- Credit Score and Eligibility: Taking a loan and repaying it on time builds your credit profile positively. However, frequent loan applications or defaults can harm your credit score, affecting future borrowing ability. Lenders assess factors like business age, annual turnover, credit history, and financials.

- Lender Reputation: Choose a lender known for transparent policies, fair practices, and good customer support. Check online reviews, ratings, and terms and conditions carefully to avoid future disputes or surprises.

What are 5 C’s of Credit ?

The 5 C’s of Credit are key criteria that lenders use to evaluate a borrower’s creditworthiness before approving a loan. Here’s a brief explanation of each:

Character:

Refers to the borrower’s credit history, reputation, and trustworthiness. Lenders assess this through credit scores, past repayment behavior, references, and overall financial conduct.

Capacity:

Evaluates the borrower’s ability to repay the loan. This includes analyzing income sources, cash flow, debt-to-income ratio, and overall financial health to ensure the borrower can meet future obligations.

Capital:

Refers to the borrower’s personal or business investment in the venture or asset. A higher level of capital contribution indicates commitment and reduces the lender’s risk.

Collateral:

Assets pledged by the borrower to secure the loan. Collateral provides assurance to the lender that, in case of default, they can recover their money by selling the pledged asset.

Conditions:

Includes the terms of the loan (amount, interest rate, tenure) and external factors like the borrower’s industry, market conditions, and the purpose of the loan, which may impact repayment ability.

Case Study: Lenskart – Structured Term Loan for Business Expansion

Lenskart Solutions Pvt. Ltd., a prominent player in the retail and e- commerce sector, secured a term loan of ₹100 crores from HDFC Bank. The loan was structured to support the company’s strategic initiatives and expansion plans, providing long-term capital for business growth.

Background & Challenge:

Lenskart needed funds to scale its retail footprint, invest in manufacturing, and expand its tech infrastructure. They wanted to avoid unnecessary equity dilution and opted for debt financing.

Key Considerations Applied:

- Interest Rate & Charges: Chose a fixed-rate term loan with a clear repayment schedule and no hidden charges.

- Loan Tenure: Opted for a 5-year repayment tenure suited to their investment timeline.

- Collateral: Secured the loan against fixed assets created through the investment.

- Lender Reputation: Chose a reputed private bank known for its structured MSME and startup lending products.

- Repayment Flexibility: Included part-prepayment options without penalty, allowing for early repayment if revenue scaled quickly.

Outcome:

Lenskart efficiently expanded into Tier-2 cities and strengthened its back-end, all without compromising equity or control. The loan was repaid partly ahead of time, strengthening its creditworthiness.

Strategic Fit & Summary:

A structured term loan complements Lenskart’s aggressive equity-backed expansion by:

- Reducing equity dilution while financing capex.

- Providing predictable repayment terms and control retention.

- Leveraging strong cash flows and manufacturing assets as collateral.

- Enabling scalable growth across new geographies and verticals.

Government Schemes and Special Programs

- MUDRA Scheme (PMMY): It Offers collateral-free loans up to ₹10 lakhs to micro and small businesses under Shishu, Kishor, and Tarun categories. And it also Supports startups, shopkeepers, and self-employed individuals through banks and MFIs.

- CGTMSE (Credit Guarantee Fund Trust for MSEs): This programme provides collateral- free credit guarantees for MSME loans up to ₹5 crores. It also encourages banks to lend to small businesses with limited assets.

- Stand-Up India Scheme: This scheme Facilitates loans from ₹10 lakhs to ₹1 crore for SC/ST and women entrepreneurs. It supports greenfield projects in manufacturing, trading, and services.

- PMEGP (Prime Minister’s Employment Generation Programme): It offers subsidies and loans for individuals to set up micro-enterprises in rural and urban areas. It covers up to ₹25 lakhs for manufacturing and ₹10 lakhs for services.

Conclusion

Choosing the right business loan is not just about securing funds, but about securing them wisely. An ideal deal balances affordability, flexibility, and speed while aligning with your business goals. By carefully evaluating key factors like interest rates, tenure, collateral, and lender credibility, businesses can ensure sustainable growth without financial strain.