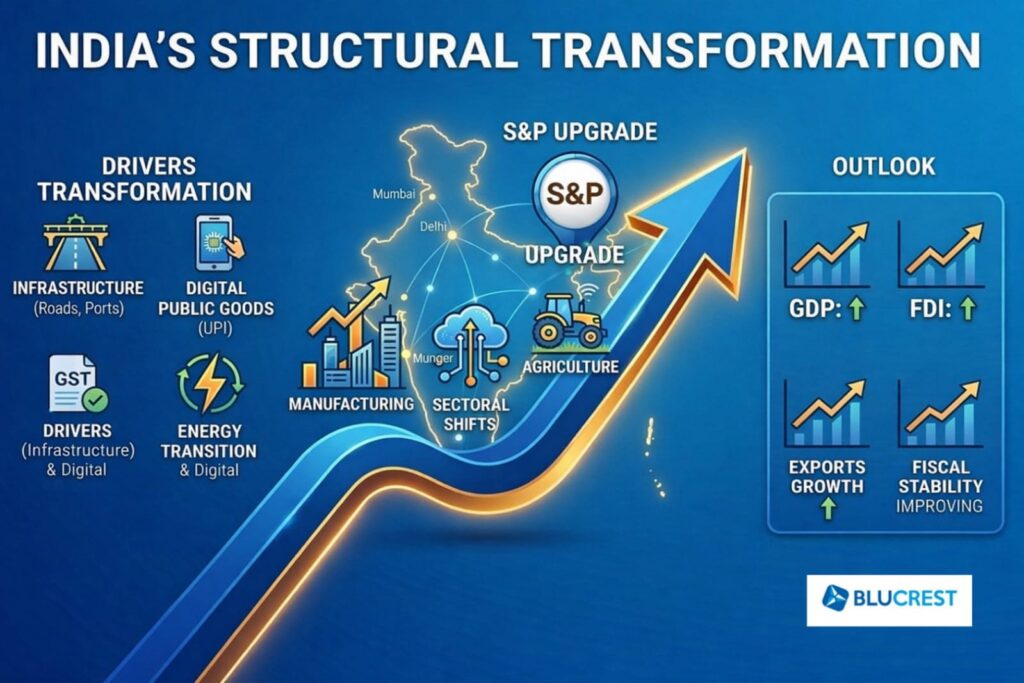

India’s economy is undergoing a significant structural transformation, reinforced by S&P Global Ratings’ recent upgrade in growth outlook. S&P raised India’s FY26 GDP forecast to 7.1%, reflecting strong economic resilience despite global uncertainties. The revision underscores India’s improved fiscal discipline, robust macroeconomic management, and growing investor confidence. A key milestone was S&P’s upgrade of India’s sovereign rating to ‘BBB’, marking stronger credibility in global markets. These developments highlight India’s strengthened economic fundamentals, sustained reform momentum, and rising position as a leading growth engine in the Asia-Pacific region.

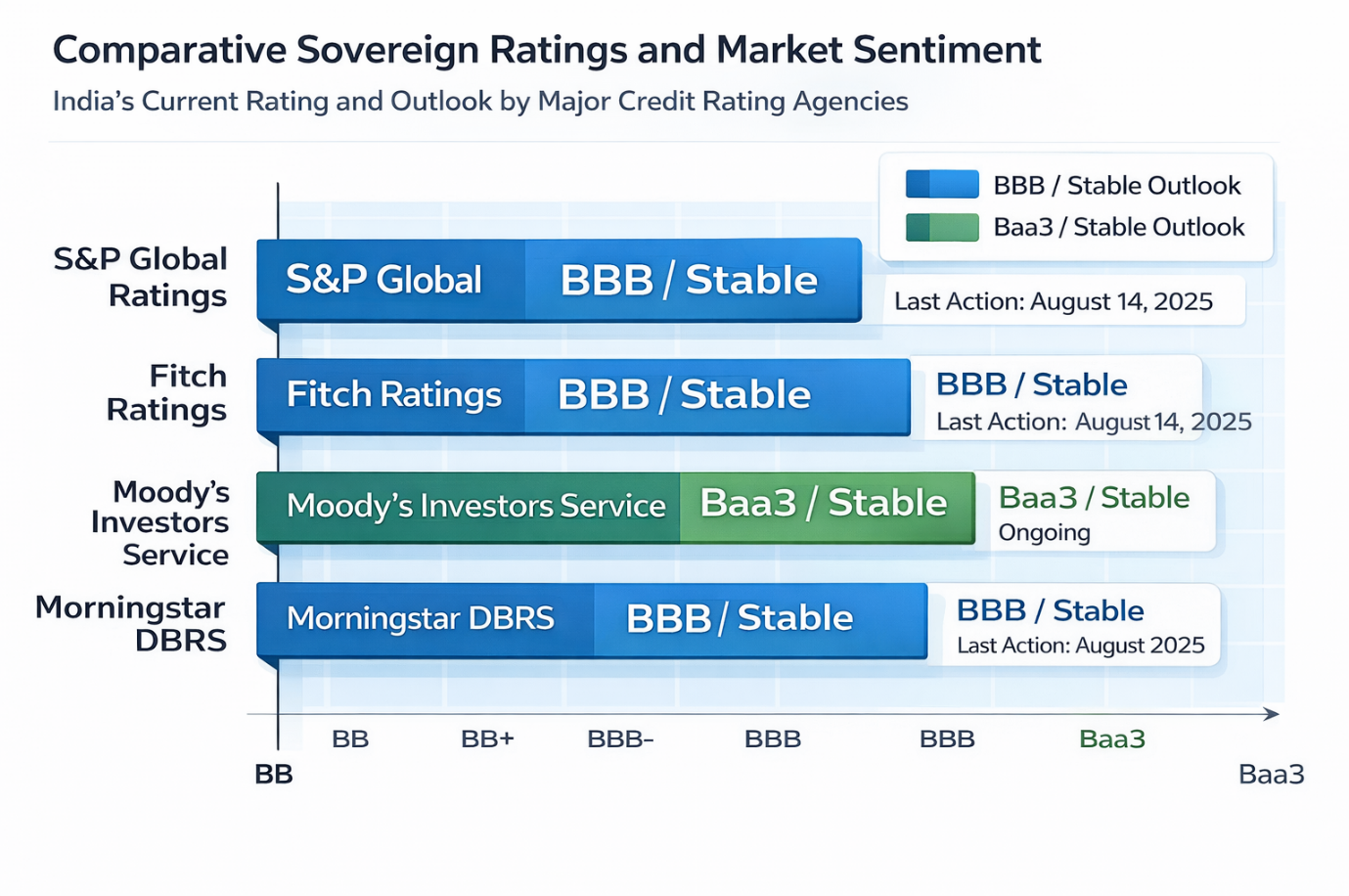

Comparative Sovereign Ratings and Market Sentiment

India’s sovereign rating outlook is improving, with S&P upgrading the country to ‘BBB’ with a stable outlook, signaling stronger fiscal credibility and economic resilience. While Fitch and Moody’s maintain their current ratings with stable outlooks, analysts note that S&P’s upgrade increases the likelihood of similar positive actions by other agencies. The announcement boosted market sentiment, leading to lower bond yields and increased foreign investor interest. This shift reflects India’s progress in fiscal consolidation, improved debt metrics, and a stronger macroeconomic foundation.

The transition to a ‘BBB’ rating is particularly noteworthy when viewed against the backdrop of historical fiscal challenges. S&P had previously elevated India to investment grade at ‘BBB-‘ in 2007. The eighteen-year gap before the next upgrade underscores the rigorous standard applied to India’s fiscal metrics, specifically the debt-to-GDP ratio and the general government deficit. Despite pandemic-era deficits reaching 9% to 13% of GDP, the government’s subsequent “calibrated fiscal strategy” has successfully brought the central deficit down to 4.4% for the fiscal year 2025-26, with a further target of 4.3% for the fiscal year 2026-27.

Decoding the 7.1% Growth Forecast: Drivers and Constraints

This text analyzes the key drivers behind India’s projected 7.1% economic growth for the 2026-27 fiscal year. It highlights how resilient domestic demand-fueled by factors like formal sector wage growth, a rebound in rural consumption, and targeted government welfare schemes-is acting as the primary engine keeping India the fastest-growing major economy despite a slight moderation from the previous year.

Investment Cycles and Public Capital Expenditure

India’s sovereign rating outlook is improving, with S&P upgrading the country to ‘BBB’ with a stable outlook, signaling stronger fiscal credibility and economic resilience. While Fitch and Moody’s maintain their current ratings with stable outlooks, analysts note that S&P’s upgrade increases the likelihood of similar positive actions by other agencies. The announcement boosted market sentiment, leading to lower bond yields and increased foreign investor interest. This shift reflects India’s progress in fiscal consolidation, improved debt metrics, and a stronger macroeconomic foundation.

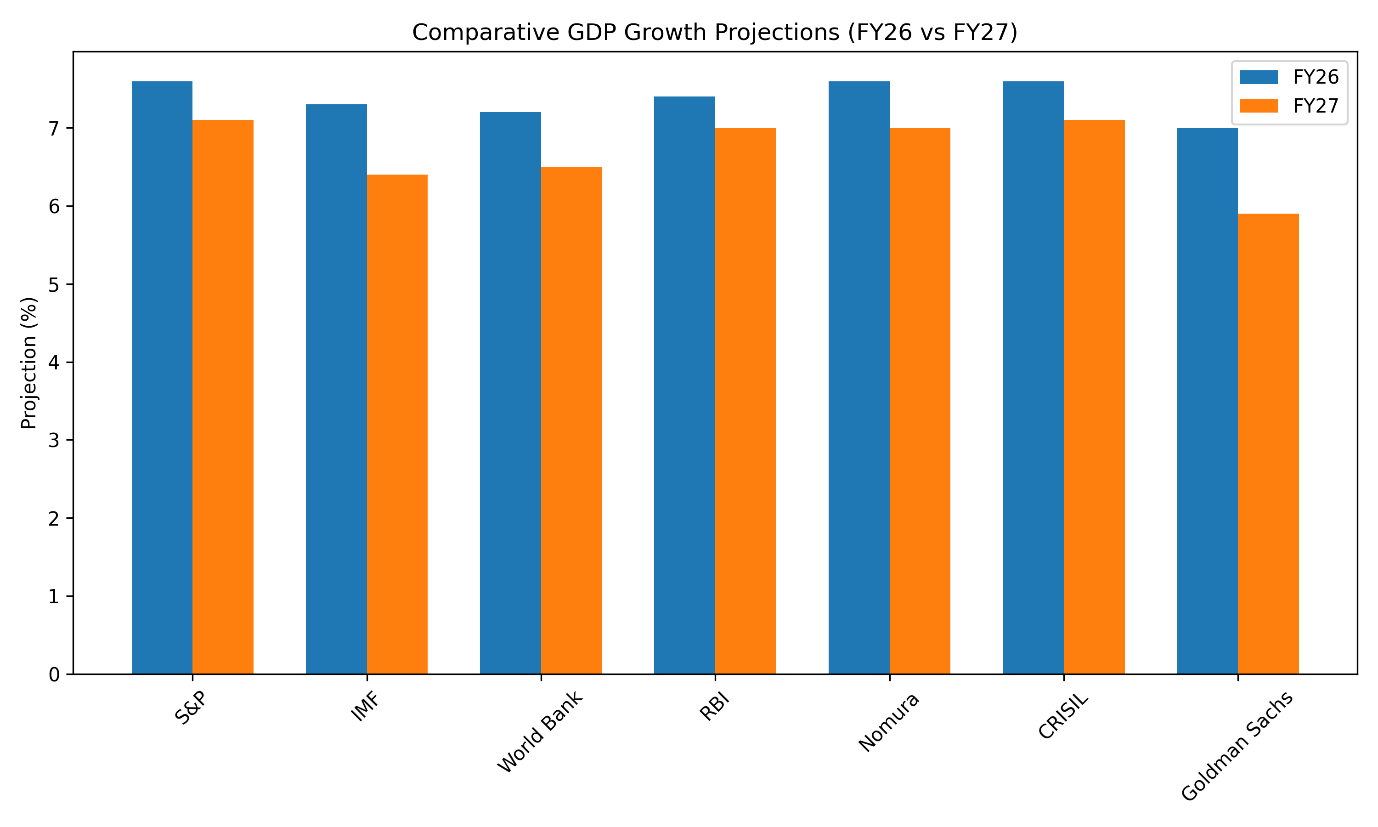

Comparative Global and Regional Projections

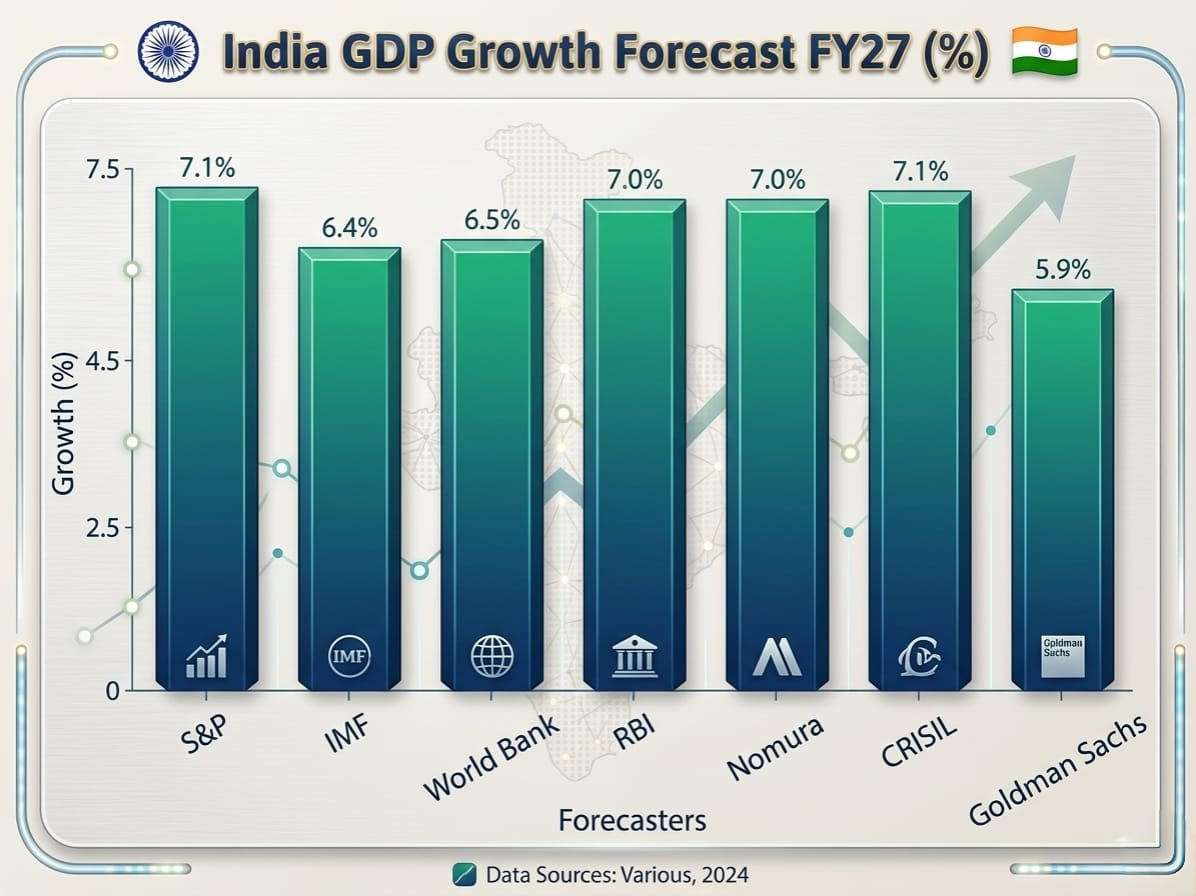

India’s growth outlook remains strong, with global and domestic agencies projecting healthy GDP momentum for FY26 and FY27. While S&P Global Ratings remains the most optimistic, forecasting stable investment-led growth, institutions like the IMF and World Bank expect moderation due to cyclical and external factors. Domestically, RBI projects steady demand support and resilient economic activity, reinforcing confidence in India’s medium-term growth trajectory.

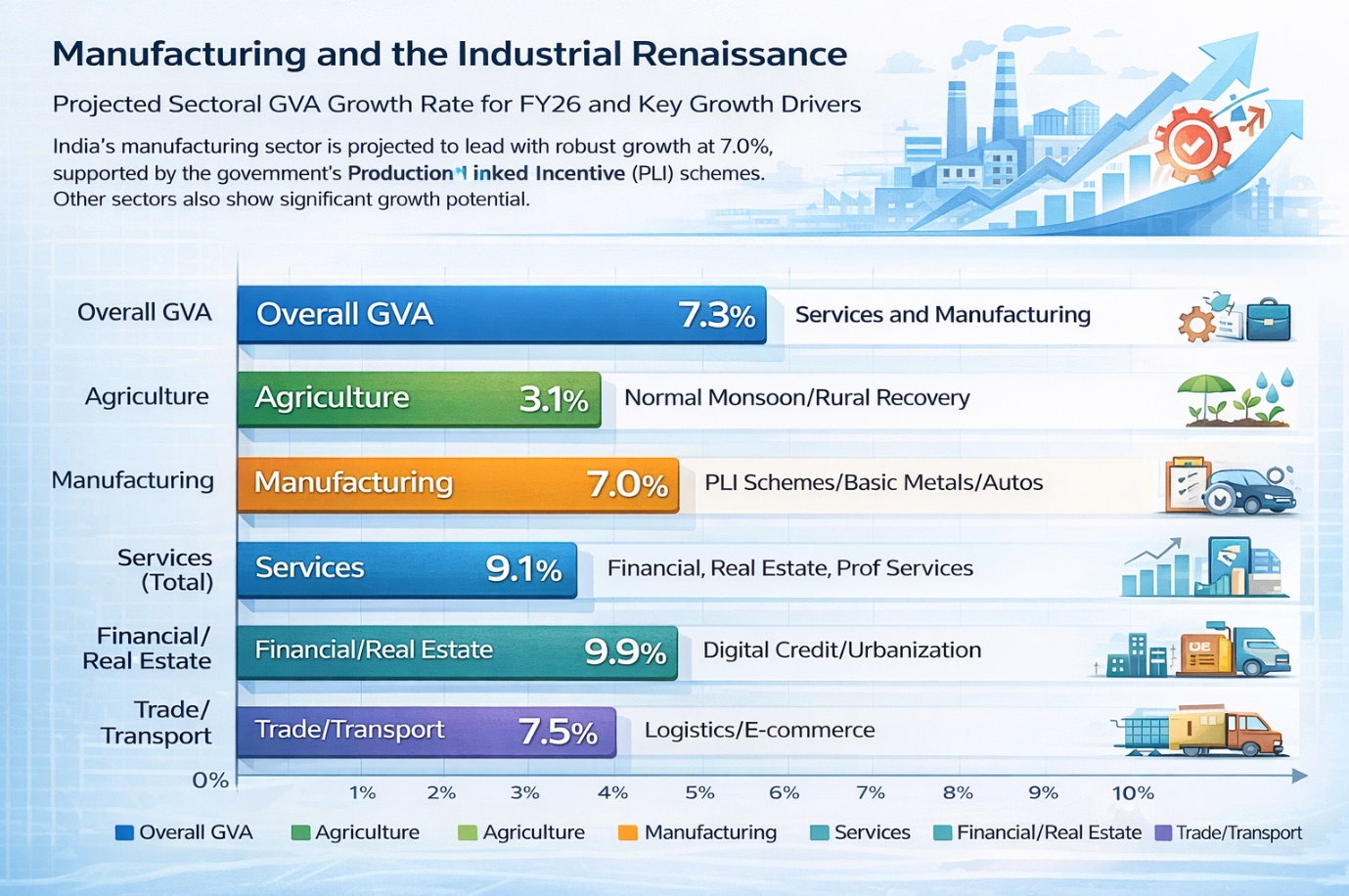

Sectoral Performance: The Rise of High-Tech Services and Manufacturing

The structural shift in the Indian economy is most evident in its sectoral composition. The services sector remains the primary growth engine, expanding by an estimated 9.1% in the fiscal year 2025-26 and maintaining strong momentum into the next year.Within services, financial and professional services have outperformed, with growth rates near 9.9%, driven by the expansion of digital lending and a burgeoning real estate market.

The Technology and AI Boom

The technology sector is undergoing a profound transformation, moving beyond traditional software services toward high-value areas like Artificial Intelligence (AI) and data center infrastructure. S&P Global economist Vishrut Rana identifies the “global boom in AI investment and data centre construction” as a significant driver for Indian activity. India is well-positioned to benefit from this trend, given its deep pool of technical talent and its growing footprint in global technology supply chains. Furthermore, currency dynamics have provided a short-term tailwind for the IT sector. BofA Securities predicts that a weaker rupee will add approximately 100 basis points to the profits of Indian IT companies. Companies like Infosys and HCL Technologies are strategically reinvesting these currency gains into R&D and strategic acquisitions, such as HCLTech’s deal for certain Hewlett Packard Enterprise assets, to strengthen their competitive positioning for the fiscal year 2026-27.

Manufacturing and the Industrial Renaissance

India’s manufacturing and industrial sector is strengthening, with GVA growth expected to reach 7% in FY26. The momentum is driven by PLI schemes, rising capital goods demand, and strong recovery in services and manufacturing. Strategic sectors like semiconductors, EVs, and biopharma are expanding rapidly, supported by higher investments and technological upgrades. Despite temporary dips in private capex, high-frequency indicators show firming investment demand and broad-based industrial improvement.

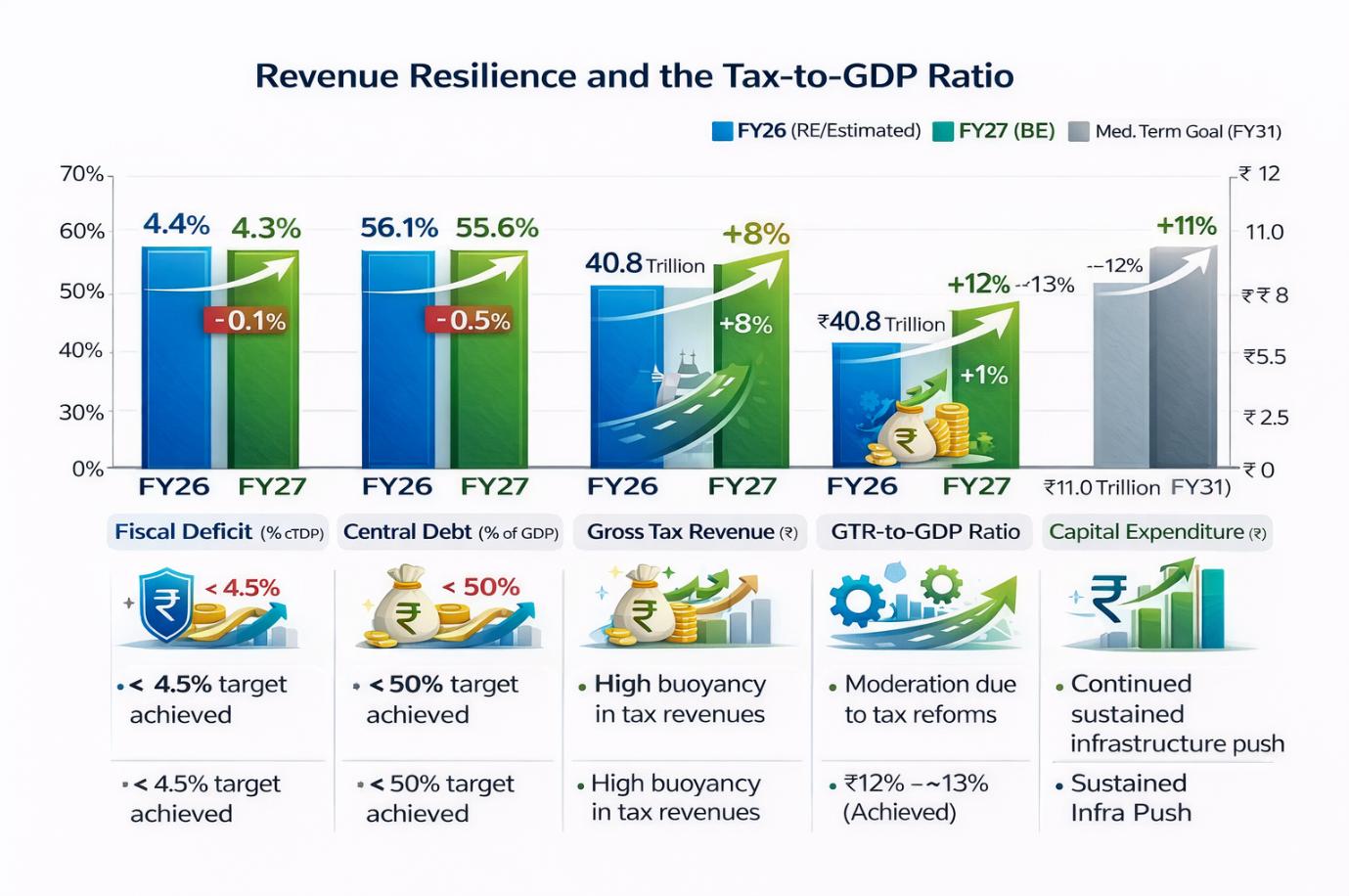

Fiscal Policy and the Debt Glide Path: The Road to 4.3%

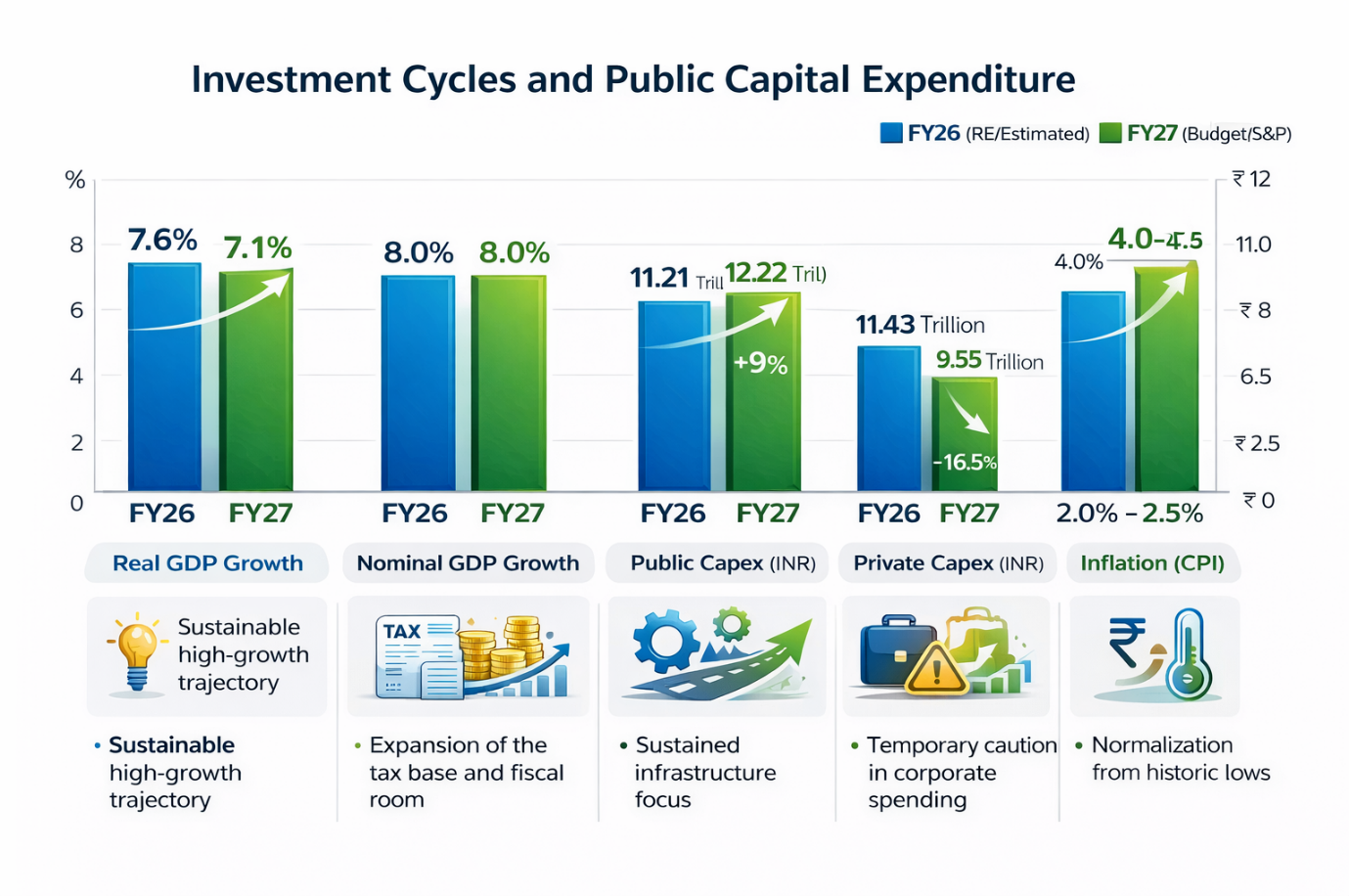

The Indian government’s fiscal strategy for the fiscal year 2026-27 continues to balance growth support with the need for long-term sustainability. The fiscal deficit for the fiscal year 2025-26 is estimated at 4.4% of GDP, successfully meeting the target established in previous budgets. For the upcoming fiscal year 2026-27, the Finance Minister has set a target of 4.3%, signaling a “calibrated” rather than abrupt consolidation.

This fiscal discipline is guided by a new “debt glide path” introduced in the 2025-26 Budget, which prioritizes the reduction of the central government’s debt-to-GDP ratio toward a target of 50 pm 1% by the fiscal year 2030-31. In the near term, the debt-to-GDP ratio is projected to decline from 56.1% in the current year to 55.6% in the fiscal year 2026-27. A declining debt ratio is critical for freeing up fiscal resources for priority sectors by reducing the government’s interest payment burden.

Revenue Resilience and the Tax-to-GDP Ratio

India’s ability to fund high infrastructure spending while reducing its fiscal deficit is supported by strong and resilient tax revenues. Gross tax revenue for FY27 is projected to rise significantly, driven mainly by direct taxes and improved compliance. Despite a slight moderation in the tax-to-GDP ratio due to recent tax reforms, overall revenue buoyancy remains strong. The government is offsetting revenue challenges through higher non-tax receipts and a conservative divestment strategy, while maintaining its medium-term goal of lowering deficits and sustaining capital expenditure growth.

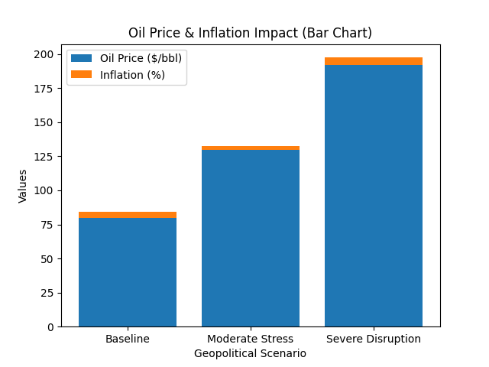

The Oil Price Wildcard

This analysis outlines external economic “wildcards” that pose downside risks to India’s projected 7.1% growth. It highlights two primary threats: India’s vulnerability to global oil price spikes caused by geopolitical tensions in West Asia, and the ongoing uncertainty surrounding global trade, particularly regarding U.S. tariffs on Indian exports.

Monetary Policy: A Delicate Balancing Act

The Reserve Bank of India (RBI) faces a complex task in the fiscal year 2026-27. While headline inflation fell to historic lows in 2025, the central bank expects a normalization toward the 4% target as base effects wane. Most analysts expect the RBI to hold interest rates steady at 5.25% in the near term, maintaining a “neutral” stance as it balances growth support with the need to contain energy-driven price pressures.

However, the “bar to hike is high,” according to Nomura, given the cyclical recovery currently underway. S&P suggests that if inflation demonstrates persistence, the RBI may implement asingle 25 basis point rate hike in the second half of the fiscal year 2026-27. The effectiveness of monetary policy will depend on the “transmission of policy rate changes” to the broader credit market, which has been uneven in previous cycles.

Conclusion: The Road to 2030

The upward revision of India’s growth forecast by S&P Global Ratings to 7.1% is a testament to the country’s emergence as a “bright spot” in a volatile global economy. The narrative of the Indian economy in the fiscal year 2026-27 is one of structural resilience, underpinned by a historic surge in private consumption, a record-breaking public infrastructure push, and a rapid pivot toward the technological frontier of AI and semiconductors. India is on track to become the world’s third-largest economy by the fiscal year 2030-31, provided it can successfully navigate the energy and trade “wildcards” presented by the global geopolitical environment.

The government’s commitment to fiscal discipline-targeting a deficit of 4.3% and a declining debt-to-GDP ratio-has earned the country its first sovereign upgrade in nearly two decades, creating a more stable environment for both domestic and foreign investment. As the global community shifts its focus toward a post-pandemic steady state, India’s growth story remains a compelling example of how a large, domestic-demand-led economy can transform external challenges into opportunities for structural reform and long-term expansion. The “Resurgent Elephant” is not just moving; it is accelerating with a renewed institutional and structural confidence.