Prologue

- ₹1.9 lakh crore+ worth of invoices have been discounted on TReDS platforms cumulatively by FY 2025, with over ₹48,000 crore transacted in FY 2024–25 alone.

- More than 80,000 MSMEs are registered on TReDS, with a 20% YoY growth in participation driven by awareness and government initiatives.

- Over 80 financiers, including major banks and NBFCs, offer invoice discounting on TReDS at competitive rates averaging 5%–8% per annum.

What is TReDS?

The Trade Receivables Discounting System (TReDS) is an RBI-regulated digital platform designed to facilitate the financing of trade receivables for Micro, Small, and Medium Enterprises (MSMEs). It enables MSMEs to sell their invoices raised on large corporates, public sector undertakings (PSUs), and government departments to banks and NBFCs at competitive rates through transparent online bidding. By allowing early payment of invoices without the need for collateral, TReDS helps address the persistent issue of delayed payments to MSMEs, thereby improving their liquidity and working capital management. The platform not only benefits small businesses but also streamlines the payment cycle for corporates and creates a low-risk lending opportunity for financiers.

Background and Regulatory Framework of TReDS

The concept of TReDS was developed to address a major pain point for India’s Micro, Small and Medium Enterprises (MSMEs): delayed payments from buyers. MSMEs often wait 60– 90 days or more to receive payment for goods or services supplied, which strains their working capital. Traditional bank loans are not always accessible or affordable for these small businesses.

To solve this, the Reserve Bank of India (RBI) proposed an electronic platform that could:

- Help MSMEs access short-term credit.

- Encourage formal, transparent, and digital invoice discounting.

- Promote financial inclusion without adding to the debt burden of MSMEs.

This idea took shape with the introduction of TReDS in 2014, and the first platforms became operational in 2017.

Regulatory Framework

The TReDS platform operates under a strong regulatory framework defined by the RBI:

1. RBI Guidelines – 2014

- RBI issued a framework for setting up and operating TReDS under the Payment and Settlement Systems Act, 2007.

- Only entities authorized by RBI can operate a TReDS platform.

2. Eligibility Criteria for TReDS Operators:

- Must be a company incorporated in India.

- Minimum paid-up equity capital: ₹25 crore.

- Must meet technology and risk management standards set by RBI.

3. Licensing:

RBI has granted licenses to three entities to operate TReDS platforms:

- RXIL (Receivables Exchange of India Ltd)

- Invoicemart (A.TReDS Ltd)

- M1xchange (Mynd Solutions)

4. Participants Defined by RBI:

- MSME Sellers

- Corporate and Government Buyers

- Banks and NBFCs (Financiers)

- No direct participation by individuals or foreign entities.

5. Mandatory Registration for Large Buyers:

- As per a Ministry of MSME notification (Nov 2020), companies with a turnover of more than ₹500 crore are mandated to register on TReDS.

6. Digital Ecosystem Push:

- RBI and the Government of India are promoting initiatives like GEM Sahay and Samarth to integrate public procurement and MSME financing via TReDS.

7. Legal Validity of Digital Transactions:

- TReDS platforms ensure e-KYC, digital signatures, and audit trails to meet the standards under the Information Technology Act, 2000 and other applicable laws.

Objectives of TReDS (Trade Receivables Discounting System)

The TReDS platform was established with the aim of strengthening the financial ecosystem for Micro, Small, and Medium Enterprises (MSMEs) by facilitating smoother and faster access to working capital. The key objectives are as follows:

How TReDS Works – Process Flow

TReDS is an online platform regulated by the Reserve Bank of India (RBI) that facilitates the financing of trade receivables (invoices) of Micro, Small and Medium Enterprises (MSMEs) from corporates and government departments through factoring or bill discounting by financiers (banks and NBFCs). Here’s the detailed step-by-step process:

Key Participants of TReDS Platform

1. MSME Suppliers:

- Who they are: Micro, Small, and Medium Enterprises that supply goods or services.

- Role: Upload invoices raised against large buyers to get early payment.

- Benefit: Receive immediate working capital by discounting receivables.

2. Corporate Buyers:

- Who they are: Large private or public sector companies, PSUs, and government departments.

- Role: Accept invoices digitally, confirming the payment obligation.

- Benefit: Better vendor relationships and improved procurement credibility.

3. Financiers:

- Who they are: Banks and NBFCs registered with the platform.

- Role: Bid to purchase (discount) invoices and provide funds to MSMEs.

- Benefit: Earn returns through discounting fees and build low-risk loan portfolios backed by buyer creditworthiness.

4. Reserve Bank of India (RBI):

- Who they are: The regulator and policymaker.

- Role: Licenses and supervises TReDS platforms, ensures fair practices, and mandates MSME invoice clearance.

5. TReDS Platform Operators:

- Who they are: RBI-licensed digital platforms like:

- RXIL (Receivables Exchange of India Ltd.)

- Invoicemart

- M1xchange

- Role: Facilitate end-to-end digital process — registration, invoice uploading, bidding, payment, and reporting.

- Benefit: Commission-based revenue from each transaction.

TReDS Analysis

1. MSMEs Registered:

- The number of MSMEs registered on the TReDS platform has seen steady growth since its inception. As of recent reports, over 70,000 MSMEs have registered across the three RBI-approved platforms — RXIL, Invoicemart, and M1xchange. This increasing registration reflects growing awareness among small businesses about the benefits of TReDS, such as faster access to working capital, reduced dependency on informal credit, and a transparent financing mechanism. The push from the government and regulators, along with mandatory buyer registration for large corporates, has further encouraged MSMEs to join the platform and take advantage of its digital and collateral-free receivables financing system.

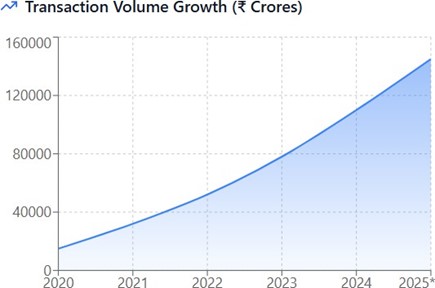

2. Transaction Volume Trends:

- Exponential Early Growth: The steepest growth occurred between 2020-2022, with volumes more than tripling.

- Maturing Market: Growth rate is moderating from 113% (2021) to projected 32% (2025), indicating market maturation.

- Consistent Upward Trajectory: Despite slowing growth rates, absolute volumes continue increasing steadily.

3. Year-on-Year Growth of TReDS in India:

- TReDS has witnessed impressive year-on-year growth in India, with invoice financing volumes rising by over 62% and transaction value increasing by 80% in FY 2023–24 compared to the previous year. The total value of discounted invoices reached ₹1.38 lakh crore, up from ₹76,645 crore in FY 2022–23. Leading platforms like RXIL and M1xchange have recorded 100%+ growth, reflecting rising MSME participation and strong adoption driven by digital integration and regulatory support.

4. Buyer and Financier Base:

- TReDS has seen expanding participation from both corporate buyers and financiers, strengthening its role in MSME financing. As of mid-2024, leading platform M1xchange had onboarded over 412 active corporate buyers, including major PSUs and government entities, and around 60 banks and NBFCs offering invoice discounting services.

TReDS Platforms Overview

The Reserve Bank of India (RBI) has authorized three digital TReDS platforms to operate in India. These platforms facilitate the online discounting of invoices for MSMEs by connecting them with buyers and financiers.

1. Receivables Exchange of India Ltd. (RXIL)

- Launch & Ownership: India’s first TReDS platform, launched in February 2016 as a JV of SIDBI, NSE, SBI, ICICI Bank & Yes Bank.

- Scale & Reach: Over 25,000 MSMEs onboarded; processed more than ₹1 lakh crore across 50 lakh invoices; monthly throughput ~₹6,000 crore. Targeting ₹75,000 crore in FY 25.

- Features & Impact: Completely digital, paperless system—MSMEs save 40–50% in financing costs. It has also partnered with state governments to enable prompt payments to MSME vendors.

- Profitability: First among peers to break even, operating at low transaction fee.

2. M1xchange (Mynd Solutions Pvt Ltd.)

- Platform Strength: RBI-licensed TReDS with 60+ financiers and 2,500+ corporates; servicing MSME-to- MSME invoice discounting too.

- Growth Metrics: Discounted ₹43,000 crore in FY 24 (86% YoY growth); ₹32,000 crore in H1 FY 25—100% YoY rise—onboarded 10,000 MSMEs and 200+ corporates.

- Sector Coverage & Offerings: Active in sectors like infra, auto, agro, telecom. Offers global expansion through “M1 NXT” and tailored solutions by industry vertical.

3. Invoicemart (A.TReDS Ltd.)

- Establishment & Partners: JV of Axis Bank and mjunction services; connects MSMEs, corporates, and financiers. It was lauched in 2017.

- Key Benefits:

- Payment within 24 hours of invoice discounting

- No collateral; PSL-accredited financing

- Seamless ERP integration and easy reconciliation

- Corporate Adoption: Active users include firms like SBI Global Factors and Sobha Ltd, citing improved vendor health and financing costs.

- Regulatory Update: Government mandate (effective Mar 2025) requires companies with turnover >₹250 crore to register and certify compliance.

Challenges of TReDS in India

- Low Participation from Buyers: Many large corporates and PSUs are reluctant to participate actively, despite government mandates. This limits invoice acceptance and reduces the attractiveness of the platform for MSMEs.

- Limited Awareness Among MSMEs: A significant portion of India’s MSMEs are either unaware of TReDS or lack digital literacy to onboard and operate effectively on the platform.

- Operational and Integration Barriers: Small businesses often struggle with uploading invoices, using digital tools, or integrating TReDS with their existing accounting or ERP systems, leading to underutilization.

Conclusion

The Trade Receivables Discounting System (TReDS) has emerged as a transformative solution for addressing the persistent liquidity challenges faced by MSMEs in India. By enabling faster, collateral-free access to working capital through a transparent and digital platform, TReDS is streamlining supply chain finance and promoting financial inclusion. Backed by strong regulatory support and growing technological integration, the platform is poised for significant expansion in the coming years. As adoption increases among MSMEs, corporates, and financiers, TReDS will play a critical role in strengthening India’s credit ecosystem, boosting MSME growth, and contributing to the overall economic development of the country.