Prologue

- India consumed approximately 120 million metric tons (MMT) of finished steel in the fiscal year 2023-2024.

- The steel trading and distribution market in India is highly fragmented, with a mix of large, organized players and numerous small, unorganized traders.

- The trading and distribution sector plays a significant role in the overall steel industry, contributing a substantial share to the revenue generated by the industry.

Overview of Steel Trading and Distribution Sector in India

Steel traders and distributors in India play a critical role in the country’s steel industry, serving as the vital link between steel manufacturers and the end-users across various sectors. These entities are responsible for the procurement, storage, and distribution of steel products, ensuring that they reach a wide range of industries including construction, automotive, infrastructure, and manufacturing.

The Indian steel market is one of the largest in the world, driven by rapid industrialization, urbanization, and large-scale infrastructure development. Steel traders and distributors are integral to this ecosystem, facilitating the movement of steel from producers to the market. The sector is highly fragmented, comprising a mix of large, organized players with extensive distribution networks and numerous small and medium-sized enterprises (SMEs) that cater to regional demands.

Growth of Steel Industry

India’s steel demand surged by 14% on a year-on-year basis during the last fiscal year, showcasing a significant divergence from global trends. This growth in India can be attributed to several factors, including robust infrastructure development, increased construction activities, and overall economic resilience. Key sectors like automotive, construction, and manufacturing have been strong drivers of steel consumption, bolstered by government initiatives such as “Make in India” and significant investments in infrastructure projects.

On the global front, steel demand contracted by approximately 1% during the same period. This decline reflects broader economic challenges faced by major economies like China, the United States, and the European Union. In China, which is the largest consumer and producer of steel globally, demand softened due to a combination of factors, including stricter environmental regulations, a cooling real estate market, and slower economic growth. The United States and the European Union also saw reduced steel demand, driven by factors such as inflationary pressures, high energy costs, supply chain disruptions, and general economic uncertainty.

The contrast between India and the global steel demand trends highlights the varying economic conditions across different regions. While India’s steel consumption is on the rise due to its expanding infrastructure and industrial base, other major economies are grappling with economic challenges that have dampened their demand for steel. This situation underscores India’s growing role in the global steel market and its relative economic resilience compared to other major economies.

In summary, India’s 14% growth in steel demand amidst a global contraction of about 1% highlights the country’s strong economic momentum and contrasts with the economic sluggishness seen in other major global economies.

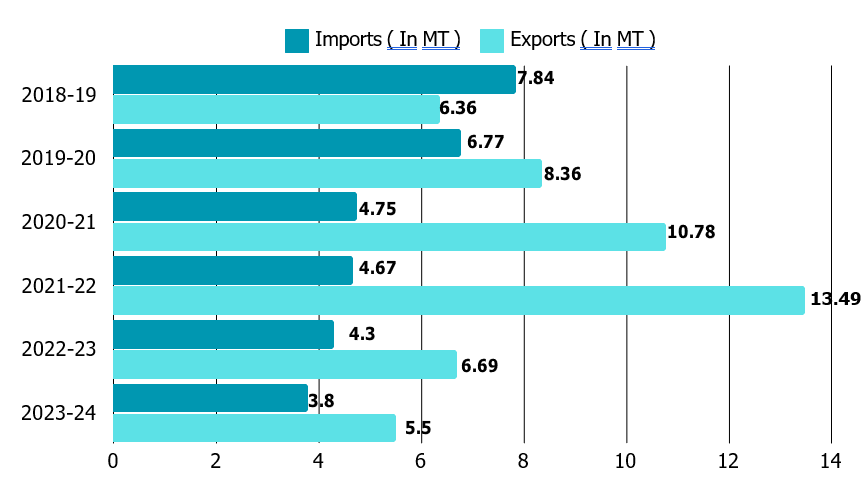

India’s Import Export of Steel

Growth of crude steel production in India has not kept pace with the growth in capacity of production, according to the report. As per this report, steel sector contributes ~2 per cent to India’s GDP and employs half a million people directly and 2 million people indirectly.

Key Observations:

- India transitioned from a net importer to a net exporter during this period.

- India solidified its position as the world’s second-largest steel producer.

- Crude steel production grew from about 103 million tonnes in 2017-18 to peak at around 120 million tons in 2021-22.

- Exports peaked in 2021-22 at 13.49 million tons.

- Imports have generally decreased over the years.

- The COVID-19 pandemic in 2020-21 saw a surge in exports due to global supply chain disruptions.

- Export duties imposed in May 2022 caused a significant drop in exports for 2022-23.

Domestic Steel Consumption: India consumed approximately 120 million metric tons (MMT) of finished steel in the fiscal year 2022-2023. Traders and distributors play a crucial role in ensuring that this steel reaches various end-user industries such as construction, automotive, and manufacturing.

Regional Distribution: Steel distribution is uneven across India, with regions like the Western and Northern states (e.g., Maharashtra, Gujarat, Punjab, Haryana) being major hubs due to high industrial activity. Southern and Eastern regions also have significant demand, particularly in states like Tamil Nadu, Karnataka, and West Bengal.

The growth of India’s steel industry over the past few years has been marked by significant expansion in production capacity, consumption, and exports. The sector has been a cornerstone of India’s industrial development, driven by robust domestic demand, government initiatives, and global market dynamics. Here’s an overview of the growth trajectory:

1. Production Growth

- Capacity Expansion: India’s crude steel production capacity has seen steady growth, reaching approximately 154 million metric tons (MMT) in 2022-2023 from around 100 MMT a decade earlier. This growth is driven by investments from both public and private sector companies, including major players like Steel Authority of India Limited (SAIL), Tata Steel, JSW Steel, and ArcelorMittal Nippon Steel India.

- Annual Production Increase: Crude steel production in India has been growing at a compound annual growth rate (CAGR) of around 5-6% over the past decade. For instance, India produced around 125 MMT of crude steel in 2022-2023, up from about 89 MMT in 2014-2015.

2. Domestic Consumption

- Rising Demand: Domestic steel consumption has consistently increased, driven by the construction, infrastructure, automotive, and manufacturing sectors. In fiscal year 2023-2024, India’s steel consumption was approximately 120 MMT, compared to around 74 MMT in 2013-2014.

- Infrastructure and Construction: The government’s focus on infrastructure development, including projects under the National Infrastructure Pipeline (NIP) and initiatives like ‘Housing for All’ and ‘Smart Cities Mission,’ has significantly boosted steel demand. The construction sector alone accounts for about 60-65% of the total steel consumption in India.

3. Export Growth

- Expanding Global Presence: India’s steel exports have grown substantially over the past few years. In fiscal year 2021-2022, India exported around 18.5 MMT of steel, a notable increase from approximately 6.6 MMT in 2015-2016. However, export volumes have been volatile due to global demand fluctuations and protectionist measures in key markets.

- Export Markets: Major export destinations include countries in Southeast Asia, the Middle East, Europe, and Africa. India has also started exporting more value-added steel products, which fetch higher margins compared to basic steel.

4. Government Initiatives and Policy Support

- National Steel Policy 2017: The Indian government’s National Steel Policy, 2017, aimed to increase India’s steel production capacity to 300 MMT by 2030-2031. The policy focuses on boosting domestic steel demand, ensuring raw material security, and encouraging exports.

- Infrastructure Investments: Significant government investment in infrastructure, including roads, railways, ports, and airports, has driven the steel industry’s growth. The Production Linked Incentive (PLI) scheme for specialty steel is also expected to further boost production and exports of high-grade steel.

5. Technological Advancements

- Modernization and Upgradation: Indian steel manufacturers have invested in modernizing plants and adopting advanced technologies, such as automation and digitalization, to improve efficiency and reduce costs. The focus has also shifted towards producing higher quality steel, including special steels for critical applications in defense, aerospace, and renewable energy sectors.

- Sustainability Initiatives: There is a growing emphasis on sustainability, with companies investing in energy-efficient technologies and reducing carbon emissions. The industry is increasingly looking at green steel production methods to align with global environmental standards.

6. Challenges and Constraints

- Raw Material Costs: Fluctuations in the prices of key raw materials like iron ore and coking coal have impacted the profitability of steel producers. India, being rich in iron ore, has an advantage, but the dependence on imported coking coal remains a challenge.

Impact on the Domestic Steel Industry

1. Increased Competition:

- Domestic Market Saturation: As new capacities are commissioned, the domestic market could become saturated, leading to increased competition among steel producers. This may force traders and distributors to engage in more aggressive pricing and sales strategies to maintain market share.

- Focus on Niche Markets: Traders and distributors might need to focus on niche markets, such as specialized steel products, to maintain profitability in a more competitive environment.

2. Pressure on Margins:

- Reduced Profitability: The combination of increased domestic supply and potential downward pressure on prices could squeeze margins for traders and distributors. This might push them to optimize operations, reduce costs, and increase efficiency to stay competitive.

- Impact of Raw Material Costs: If raw material prices rise globally, domestic steel producers may pass on these costs to the market, which could further compress margins for traders and distributors, especially if they are unable to pass these costs on to end customers.

3. Shift in Distribution Channels:

- Direct Sales by Producers: With increased capacity, some steel producers may opt to bypass traditional distribution channels and sell directly to large consumers or end-users. This could reduce the role of intermediaries, pressuring traditional traders and distributors to offer more competitive pricing or value-added services.

- Digital Platforms: The rise of digital trading platforms could also impact traditional distribution models, enabling producers to reach customers directly and reduce reliance on physical traders and distributors.

4. Environmental Impact:

- Emissions and Sustainability: Steel production is energy-intensive and a significant source of CO2 emissions. The domestic industry faces pressure to adopt more sustainable practices, such as using electric arc furnaces (EAFs) instead of traditional blast furnaces, or recycling scrap steel. The shift towards greener technologies can be costly but necessary for long-term viability.

- Regulatory Pressure: Environmental regulations aimed at reducing emissions and improving sustainability can increase operational costs for steel producers. Compliance with these regulations often requires investment in new technologies or processes.

5. Technological Impact:

- Innovation: The domestic steel industry is increasingly adopting advanced technologies such as AI, automation, and IoT to improve efficiency and reduce costs. These innovations can help domestic producers remain competitive in the global market.

- R&D Investments: Investment in research and development is crucial for the domestic steel industry to develop new steel grades, improve production processes, and reduce environmental impact.

Investments

According to the data released by the Department for Promotion of Industry and Internal Trade (DPIIT), between April 2000-March 2024, Indian metallurgical industries attracted FDI inflows of US$ 17.51 billion. In FY22, demand for steel was expected to increase by 17% to 110 million tonnes, driven by rising construction activities.

Some of the major investments in the Indian steel industry are as follows:

- In February 2024, The JSW Group is set to build a steel plant in Jagatsinghpur, Odisha, with an investment of US$ 7.8 billion (Rs. 65,000 crore). The plant will have a production capacity of 13.2 million tons of steel per year and is expected to create 30,000 jobs.

- In February 2024, JSW Steel plans to establish a joint venture with Japan’s JFE Steel Corporation in a 50:50 partnership to invest US$ 661.9 million (Rs. 5,500 crore) in setting up a plant in Karnataka.

- In January 2024, according to Mr. Lakshmi Mittal, Gujarat will host the world’s largest steel manufacturing site by 2029 at the Vibrant Gujarat Summit

- In November 2023, Steel Secretary Mr. Nagendra Nath Sinha said that India’s steel capacity has crossed 161 million tonnes (MT), and the industry is poised for continuous growth.

- In October 2023, Government e-Marketplace, the national public procurement platform, signed a memorandum of understanding (MOU) with the Indian Steel Association (ISA). This partnership intends to bring all ISA members onto the GeM platform as sellers, promoting a diverse business environment regardless of their size.

- In July 2023, Union Minister Mr. Jyotiraditya Scindia announced that Japan is eager to invest ¥ 5 trillion (US$ 36 billion), in various sectors in India, including steel.

- As announced in May 2023, INOX Air Products will invest Rs. 1,300 crore (US$ 157.5 million) to set up two air separation units having a capacity of 1,800 tonnes a day each at Tata Steel’s plant in Dhenkanal, Odisha.

- In May 2023, the industry body Indian Steel Association (ISA) announced signing an agreement with the ASEAN Iron and Steel Council (AISC) to unlock new avenues of growth and sustainability in the steel sector.

Global trade and geopolitical factors impacting the steel industry

1. Trade Policies and Tariffs:

Many countries impose tariffs to protect their domestic steel industries. For example, the U.S. imposed a 25% tariff on steel imports in 2018 under Section 232, citing national security concerns. This not only reshaped global trade flows but also led to retaliatory tariffs from trading partners. Protectionist measures by countries, including the European Union and India, have disrupted international steel markets, leading to trade imbalances and changes in steel supply and demand.

2. U.S.-China Trade War:

The trade war between the U.S. and China, initiated in 2018, has significantly impacted global steel trade. Higher tariffs on Chinese steel led to China redirecting its exports to other markets, creating oversupply and price competition in regions like Southeast Asia and Africa.

3. Russia-Ukraine Conflict:

The ongoing war between Russia and Ukraine has deeply affected global steel supply chains. Ukraine, a major exporter of steel and iron ore, has faced significant production disruptions, while sanctions on Russia have reduced the flow of steel and raw materials from one of the world’s top producers. The conflict has caused steel shortages and rising prices in Europe, pushing European countries to seek alternative suppliers, which has shifted global steel trade patterns.

4. China’s Steel Production and Environmental Policies:

China accounts for over half of the world’s steel output, making its production decisions highly influential on global steel markets. Overcapacity and export of cheap steel from China have led to trade tensions and oversupply in global markets. China’s efforts to reduce steel production to curb pollution and meet environmental goals have impacted global supply and driven up steel prices. As China moves towards reducing carbon emissions, its steel exports fluctuate, affecting global trade.

5. Supply Chain and Logistic Disruptions:

The COVID-19 pandemic disrupted global supply chains, leading to delays in the delivery of raw materials like iron ore and coking coal, which are essential for steel production. Shipping costs soared, further impacting global steel trade and pricing. Ongoing disruptions in global logistics, such as container shortages and rising fuel costs, have increased the cost of transporting steel, making international trade more expensive and less predictable.

Future Outlook

- The future outlook for India’s steel industry is robust, with strong growth anticipated due to rising domestic demand, significant capacity expansions, and supportive government policies.

- The country’s ongoing infrastructure projects, urbanization, and industrial growth are set to drive substantial increases in steel consumption.

- Major investments by key steel producers in new facilities and technological advancements, such as green steel production and digitalization, will enhance efficiency and sustainability.

- The government’s initiatives, including the Production Linked Incentive (PLI) scheme and National Steel Policy, are expected to bolster both domestic production and export potential.

- However, the industry must navigate challenges such as fluctuating raw material costs and the need for environmental compliance.

- Overall, India’s steel sector is well-positioned to become a global leader, balancing growth with sustainability and innovation.

- The Indian steel industry is expected to continue growing, with an anticipated increase in production capacity and domestic demand.

- The government’s focus on infrastructure development, urbanization, and the PLI scheme for specialty steel will be key drivers of this growth.

Conclusion

The trends in the steel industry reveal a dynamic and evolving landscape marked by several key developments. The industry is experiencing significant growth driven by increased demand from infrastructure projects and urbanization, alongside major investments in capacity expansion and technological advancements. The shift towards sustainability is reshaping production practices, with a growing emphasis on green steel technologies and decarbonization. Global trade dynamics and geopolitical factors continue to influence steel markets, creating both challenges and opportunities for producers. As the industry adapts to these trends, it is poised for continued innovation and expansion, with a focus on meeting future demand while addressing environmental and economic pressures.