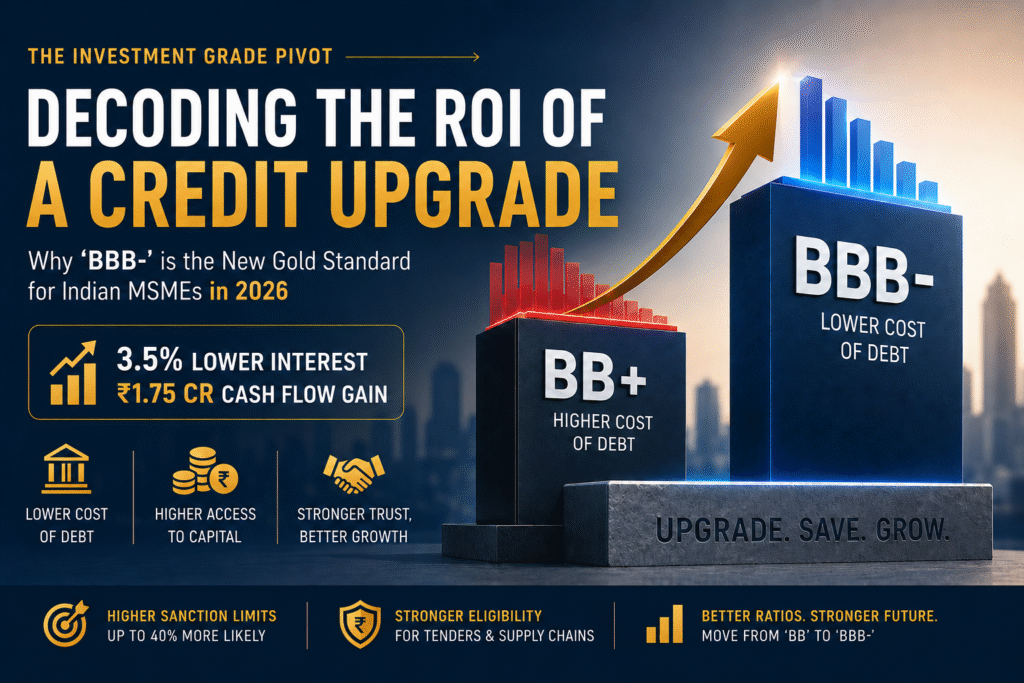

In the current Indian economic climate of 2026, a credit rating has evolved from a regulatory checkbox to a strategic profit lever. As the Reserve Bank of India (RBI) manages liquidity and interest rate cycles, the cost of capital for Indian MSMEs is increasingly dictated by their Credit Rating Notch. This report analyzes the transition from ‘BB+’ (Speculative Grade) to ‘BBB-‘ (Investment Grade) and the massive Return on Investment (ROI) this pivot provides to a mid-market enterprise.

The Quantitative Impact: The “Rating Spread” Analysis

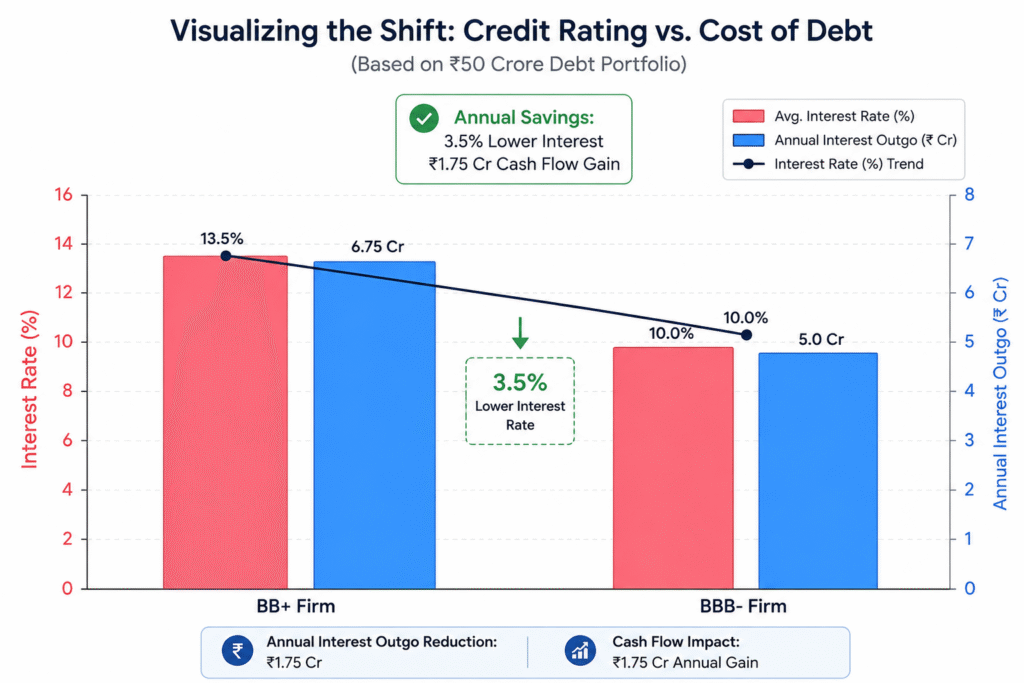

The most immediate benefit of a credit upgrade is the reduction in the Risk Premium charged by lenders.

Interest Rate Divergence (Estimates for 2026)

- BB+ Category (Speculative): Typically viewed as high-risk. Borrowing costs often range between 13.5% and 6.75%. Access to capital is often restricted to NBFCs and smaller private banks.

- BBB- Category (Investment Grade): This is the “Entry Level” for institutional investors and Tier-1 banks. Borrowing costs drop significantly to 10.0% – 5.0%.

Strategic Insight: Over a 5-year term loan, a simple move to ‘BBB-‘ saves the firm ₹3.5% Crores in interest alone-capital that could fund an entirely new production line or a digital transformation project.

The chart above illustrates the Cliff Effect: once a firm crosses the threshold into the ‘BBB-‘ category, the cost of debt doesn’t just decline; it collapses, as a much wider pool of lenders (Public Sector Banks, Insurance Funds, and Mutual Funds) are legally and internally permitted to lend only to Investment Grade entities.

Why ‘BBB-‘ is the “New Gold Standard” in 2026

In 2026, several factors make the ‘BBB-‘ rating more valuable than ever:

- Supply Chain Finance: Large Corporates and OEMs are now vetting their MSME suppliers based on credit ratings to ensure supply chain stability.

- Public Procurement: New government tenders increasingly require a minimum ‘BBB-‘ rating for eligibility in high-value infrastructure and defense projects.

- Enhanced Sanction Limits: Banks are 40% more likely to approve an enhancement in Working Capital limits for ‘BBB-‘ rated firms compared to ‘BB+’ rated firms, even with the same collateral.

The “Credit Anchors” of 2026: How to Move the Needle

To achieve this pivot, BLUCREST identifies three critical metrics that rating agencies (CRISIL, CARE, ICRA) are currently prioritizing:

- Debt Service Coverage Ratio (DSCR): Aim for >1.5x. Agencies are wary of firms that are “growing too fast” at the expense of liquidity.

- Total Outside Liabilities / Tangible Net Worth (TOL/TNW): A shift toward equity or retained earnings that brings this ratio below 2.0x is often the trigger for an upgrade.

- Net Cash Accruals (NCA): Demonstrating that your operating cash flow can repay your entire long-term debt within 3 to 4 years.

Conclusion: The BLUCREST Advantage

The journey from ‘BB+’ to ‘BBB-‘ is rarely about luck; it is about financial engineering and transparent storytelling. At BLUCREST, we specialize in identifying the “low-hanging fruit” in your balance sheet-optimizing ratios and debt structures-to ensure that when you sit across from a rating agency, your story is backed by data that demands an upgrade.

Is your firm stuck in the ‘BB+’ trap? A 1% improvement in your rating could save you millions. Let BLUCREST map your path to Investment Grade.